Let's Shape The Future Of Your Investments!

Natoque iaculis cursus augue urna commodo aptent morbi tortor porttitor quis ornare.

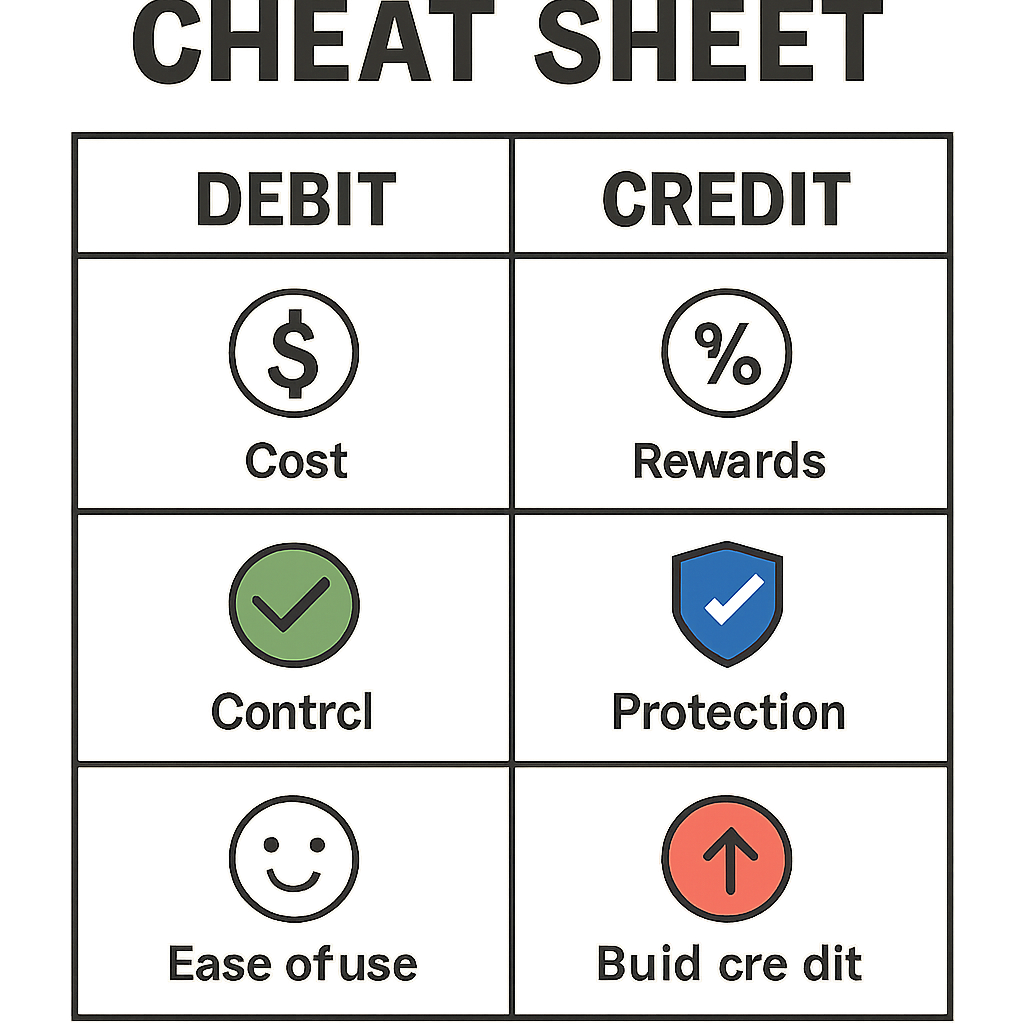

You are standing at the checkout counter staring at two similar pieces of plastic in your wallet. Physically, they look almost identical, but that simple appearance hides a massive financial difference. Swiping the wrong one could unexpectedly cost you money or leave your bank account completely unprotected.

The true difference between a debit card and a credit card comes down to one crucial question: whose money are you spending? In practice, debit means dipping into your own bucket of cash, while credit means crossing a bridge to borrow the bank’s money. Once you realize you are either spending your personal savings today or promising to pay the bank tomorrow, your entire approach to shopping will shift.

According to consumer protection laws, this daily choice impacts much more than your current grocery bill. Deciding whether to use a credit or debit card directly determines your safety against online fraud and whether you are building a positive trust profile for buying a house later.

The biggest difference between a debit and credit card isn’t the plastic itself. It’s whose money you are actually spending at the checkout counter. Think of your checking account as a bucket. When you use a debit card, you dip directly into your own bucket, scooping out your hard-earned cash instantly at the register.

Swiping a credit card, however, is like walking across a bridge to the bank’s bucket. You aren’t spending your money today; instead, the bank is giving you a short-term micro-loan for your groceries. You simply promise to walk back across that bridge next month and repay them.

This highlights the core contrast of revolving credit vs immediate fund withdrawal. A debit card requires you to have the cash upfront. Conversely, a credit card lets you borrow up to a set limit, repay it, and borrow again in a continuous cycle without needing those funds today.

Realizing whose funds are on the line changes everything about how you shop. Because the bank’s money is exposed instead of yours, consumer protections drastically shift, providing a crucial safety net against online fraud.

Imagine waking up to an alert for a $500 purchase you didn’t make. Because of the “bucket vs. bridge” dynamic, this triggers the “Timeline of Loss.” With a debit card, that money is instantly drained from your checking account, meaning your rent or grocery money is missing today while the bank investigates. With a credit card, the thief took the bank’s money, leaving your actual cash safely in your bucket.

Federal regulations treat these situations differently regarding fraud protection for unauthorized transactions. Under consumer protection laws for electronic transfers, your financial risk with a debit card depends on how fast you report the theft—wait a few days, and you could easily lose up to $500. In contrast, your legal liability for lost or stolen cards on a credit account is capped at just $50, and most modern banks will completely waive even that small fee.

This drastic difference in personal risk is exactly why credit cards are much safer for online shopping. Consider how resolving fraud actually works for the consumer:

Beyond keeping your daily cash flow secure, managing the bank’s money responsibly has a lasting impact on your financial future by building the trust profile required for future loans.

Swiping a debit card keeps you out of debt, but it does nothing to prove your reliability to future lenders. Because you are only dipping into your own bucket, banks learn nothing about your borrowing habits. A credit card flips this dynamic by reporting your on-time payments to bureaus, creating a profound impact on personal credit scores. This builds the “Trust Profile” required to secure a mortgage or car loan.

Mastering this system does not require you to owe thousands of dollars. The safest method for building credit history for beginners is assigning one small, recurring expense—like a monthly Netflix subscription—to your card and setting it to autopay. That tiny transaction writes a glowing “letter of recommendation” to credit bureaus every month without risking your daily cash flow.

Anyone starting from scratch can utilize secured cards for rebuilding credit safely. These cards function like training wheels by requiring a refundable cash deposit upfront, which becomes your borrowing limit. You still borrow and prove you can pay a monthly bill, but the bank takes on zero financial risk if you miss a payment.

Once your trust profile is established, banks will compete to offer you better terms, perks, and rewards.

Banks win your business by offering free money just for swiping. Every time you buy groceries, you can earn a percentage back through cashback rewards and travel benefits. The catch? Banks can only afford this because millions of people pay “rent” on the money they borrow.

Your secret weapon is understanding annual percentage rate (APR) so you can outsmart this system. When you carry a balance past your monthly billing cycle, you are charged this interest. However, paying your bill in full unlocks a “grace period.” During this window, your short-term loan is entirely free, letting you keep your rewards without paying a single cent to the bank.

Discovering exactly how interest charges are calculated reveals why holding debt is so expensive—carrying a $1,000 balance could cost you $20 a month just for the privilege of owing that money. To ensure your perks stay profitable, follow these three rules of the road:

While mastering these perks puts cash back in your pocket, credit cards also prevent everyday merchant headaches like temporary payment holds.

Picture checking into a hotel or swiping at the gas pump. These businesses pre-authorize your plastic for extra money to cover potential room damages or a full tank, known as incidentals. Because the exact final bill is initially unknown, the merchant places a temporary hold on your account to guarantee payment.

Handing over a debit card immediately freezes real cash inside your checking account. This invisible lock can instantly derail managing monthly spending and budgeting, making your money completely inaccessible for days. If an automated bill processes while your funds are trapped, you risk steep bank overdraft fees vs high interest rates which normally dominate credit warnings.

Swiping a credit card solves this problem entirely by placing that temporary block on the bank’s money, leaving your actual cash untouched and safe. This protective buffer is exceptionally crucial when using cards for international travel, where massive security deposits are standard. With your personal cash flow protected from unexpected merchant freezes, you are ready to apply these rules to your daily spending habits.

You’ve moved past seeing the plastic in your wallet as identical tools. By mastering the pros and cons of borrowing money versus spending your own cash, you can stop passively swiping and start using your cards as strategic financial shields.

To build your confidence, implement these actionable “Always/Never” rules:

Mastering credit vs debit isn’t about picking one universally superior card; it’s about pulling out the right tool for the exact moment. Try applying this framework to your very next purchase for immediate peace of mind. Every time you pause at the checkout counter to choose strategically, you transform a basic transaction into a calculated step toward smarter financial management.

| Feature | Debit Card | Credit Card |

|---|---|---|

| Source of Funds | Money comes directly from your bank account | Borrowed money from the card issuer |

| Credit Check Required | No | Usually yes |

| Impact on Credit Score | No impact | Can help build credit history |

| Interest Charges | None | Charged if balance is not paid in full |

| Spending Limit | Available bank balance | Credit limit set by issuer |

| Fraud Protection | Good | Usually stronger protection |

| Rewards Programs | Limited | Often includes cashback, points, or miles |

| Approval Process | Simple | Requires credit application |

| Debt Risk | Lower | Higher if balances are not managed properly |

| Best For | Budgeting and everyday spending | Building credit and earning rewards |