Let's Shape The Future Of Your Investments!

Natoque iaculis cursus augue urna commodo aptent morbi tortor porttitor quis ornare.

Determining the ideal number of credit cards can be challenging. Many factors influence this decision, including financial goals and spending habits.

Some people wonder if having multiple credit cards is beneficial. Others worry about the risks of having too many.

Credit cards can offer rewards and perks, but they also come with responsibilities. Managing them wisely is crucial to avoid debt.

Understanding the impact of credit cards on your credit score is essential. Each card affects your credit utilization and history.

This guide will help you navigate these considerations. We’ll explore the pros and cons of multiple credit cards.

By the end, you’ll have a clearer idea of how many credit cards you should have.

The number of credit cards you hold can significantly impact your financial health. Each card affects your credit score, influencing credit utilization and payment history. Managing these factors wisely is essential for maintaining a healthy credit profile.

Having more credit cards can offer financial flexibility, allowing you to take advantage of various benefits. Rewards, cashback, and travel perks can add value to your daily expenses. However, more cards also mean juggling multiple due dates and payment amounts, requiring careful organization.

On the flip side, too many credit cards can pose risks if not managed properly. Overspending and accumulating debt can become real concerns. It’s crucial to consider your financial habits before acquiring additional credit cards.

Here’s why the number of credit cards matters:

Understanding these aspects can help you decide how many cards you should possess. Balancing these pros and cons is key to optimizing your credit card portfolio.

When deciding how many credit cards to carry, consider your financial goals and spending habits. Different goals may require different strategies, such as earning rewards or building credit.

Next, assess your ability to manage payments. Juggling multiple cards means keeping track of various due dates and billing cycles. Your organizational skills will play a big role in your success.

Understanding your credit utilization ratio is vital. A low ratio can boost your credit score, so consider how more credit affects this metric. The total available credit across multiple cards can help manage this ratio effectively.

Furthermore, think about the types of benefits you want. Some cards may offer rewards for specific categories, aligning with your lifestyle. Choosing cards with compatible benefits enhances your rewards experience.

Here’s a list of factors to consider:

By analyzing these aspects, you can make informed decisions about your credit card portfolio. Balancing these considerations helps maintain a healthy financial standing while taking advantage of available benefits.

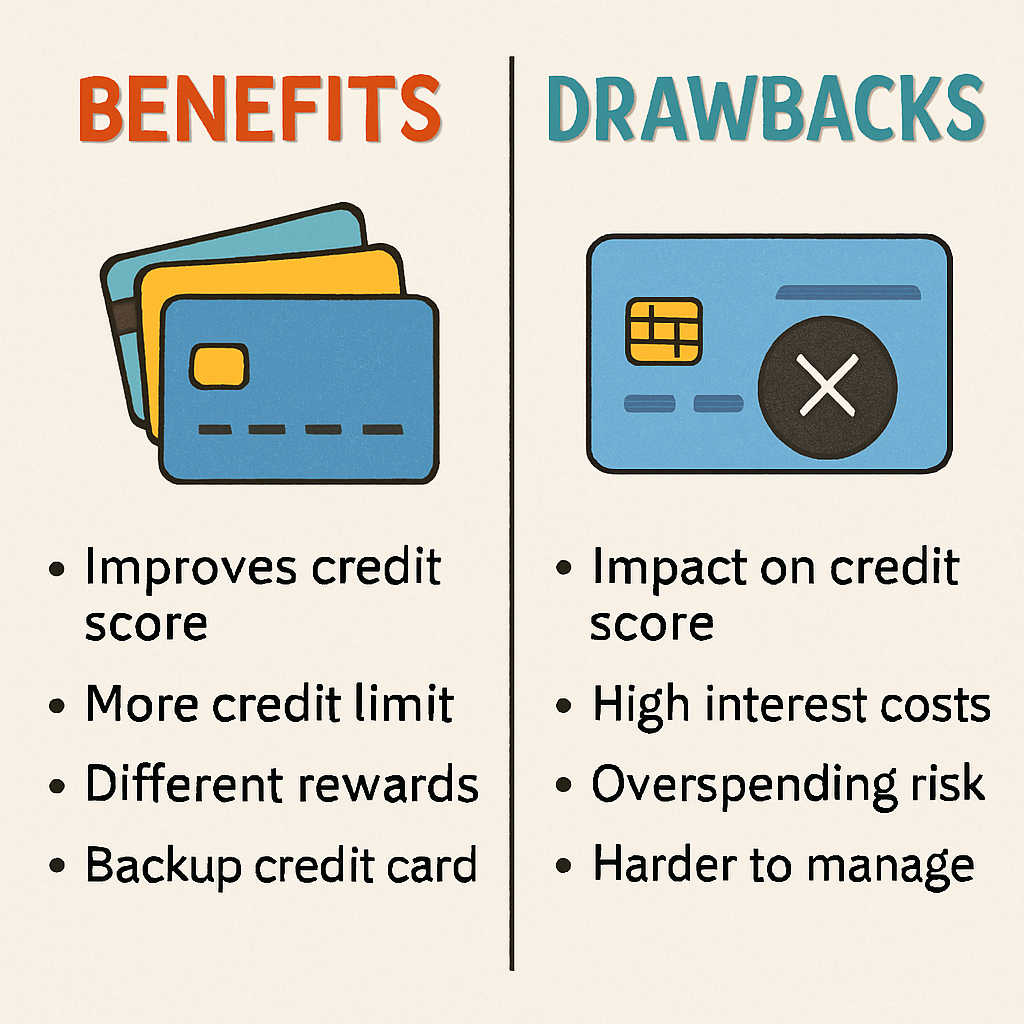

Owning several credit cards offers notable benefits but also presents challenges. One major advantage is the ability to earn diverse rewards. By holding cards with different reward structures, you can maximize benefits on various spending categories.

Another pro is the potential for improving your credit score. More credit lines can lower your credit utilization ratio, positively impacting your credit profile. Additionally, you get a financial backup during emergencies, providing a safety net when unexpected expenses arise.

However, there are significant downsides to consider. Managing multiple cards requires diligence to avoid missed payments, which harm your credit score. This responsibility can be demanding and may lead to financial stress if mishandled.

Moreover, the temptation to overspend is prevalent with increased credit limits. This risk of accumulating high-interest debt becomes more pronounced with every card. Annual fees and varying interest rates can further complicate managing costs.

Consider these pros and cons:

In weighing these factors, assess your financial habits and discipline. Striking the right balance is crucial for leveraging the advantages while minimizing potential pitfalls.

Having numerous credit cards can seem daunting. It often raises concerns about financial stability and borrowing habits. Many wonder if owning many cards is detrimental.

In reality, the impact largely depends on how you manage them. Maintaining a high number of cards is not inherently bad if handled responsibly. This includes paying balances in full each month and avoiding unnecessary charges.

Nonetheless, there are risks associated with juggling too many accounts. It can make managing payments more complex, increasing the chance of forgetting a due date. This can lead to late fees and negatively affect your credit score.

Also, the compulsion to spend more due to available credit must be managed. Assessing your personal financial behavior is key to determining the right number. Consider these factors:

Understanding your capabilities helps you decide if maintaining multiple credit cards is feasible for you.

Determining how many credit cards are too many is subjective. It varies based on personal financial habits and goals. While some people comfortably manage several cards, others may struggle with just a few.

A general rule involves considering your ability to manage payments. If you find keeping track of due dates challenging, you might have too many. Overextending yourself can lead to missed payments and high-interest rates.

Your credit utilization ratio is another important factor. A higher number of credit cards with manageable balances can positively impact this ratio. However, acquiring cards faster than you can manage can be risky. Assessing your financial discipline is crucial before deciding how many cards to carry. Reflect on these indicators:

By evaluating these factors, you can determine if your current number of cards suits you.

Financial experts often stress that there’s no one-size-fits-all answer for the ideal number of credit cards. Your financial situation, goals, and spending habits play key roles. Some financial advisors recommend having at least two credit cards for flexibility and a backup option.

Having multiple cards can offer distinct benefits. You can maximize reward points by using cards that align with specific spending categories. However, experts caution against opening too many cards at once, as it may lower your credit score temporarily due to hard inquiries.

To maintain a healthy credit profile, prioritize responsible credit management. Pay off your balances in full each month to avoid high-interest charges. Choose cards offering benefits that match your lifestyle to make the most out of them. Consider these expert tips:

by CardMapr.nl (https://unsplash.com/@cardmapr)

By considering professional advice and personal circumstances, you can optimize your credit card ownership for financial success.

Handling several credit cards demands a smart approach to ensure financial well-being. First, develop a system to keep track of payment due dates. Missing payments can lead to penalties and negatively affect your credit score.

Next, aim to keep your credit utilization ratio low. This ratio compares your credit card balances to your credit limits. Keeping it below 30% is recommended for a strong credit profile.

Understanding each card’s benefits and fees can save you money and improve financial planning. Some cards offer cash back, rewards, or travel perks. However, these are only beneficial if used wisely.

To manage your credit cards effectively, consider these strategies:

By following these guidelines, you can enjoy the perks of multiple credit cards while maintaining control over your financial health. Make informed decisions, and you’ll find credit cards can be a valuable financial tool.

Determining the right number of credit cards isn’t always clear-cut. A few indicators can help guide your decision. For instance, if you find it difficult to keep track of payments, you may have too many cards.

Conversely, if you’re often faced with spending restrictions or denied transactions, consider adding another card. A broader credit limit might improve financial flexibility and your credit utilization ratio.

Evaluate your credit card situation through these signs:

Regularly review your financial needs and habits. Adjust your credit card count accordingly to align with your current financial goals.

Navigating credit card ownership can be confusing. Many people have common questions about managing their cards. Let’s address some of these concerns to help you gain clarity.

Is it bad to have too many credit cards? It depends on how you manage them. Responsible use can positively impact your financial health.

Is it good to have multiple credit cards? Multiple cards offer flexibility and potential rewards. They can also help diversify your credit profile.

Here’s a quick list of frequently asked questions:

Understanding the nuances of credit card ownership can empower you to make informed decisions. Regularly update your knowledge to optimize credit card use.

Determining how many credit cards you should have comes down to understanding your personal financial goals and habits. There isn’t a one-size-fits-all answer because every financial situation is unique.

Assess your ability to manage payments and evaluate the benefits each card offers. With thoughtful management, credit cards can be a powerful tool in financial planning. Keep in mind that having the right number of credit cards involves balancing both responsibility and strategic benefits. Ultimately, the ideal number is one that aligns with your needs and supports your financial health.

| Question / Keyword Topic | Simple Answer | Best Recommendation | Why It Matters |

|---|---|---|---|

| How many credit cards should I have? | Most people do well with 1 to 3 credit cards | Start with one card, then add more only if you can manage payments responsibly | Having more than one card can improve rewards and credit utilization, but only if managed carefully |

| How many credit cards is too many? | Too many is when you cannot track payments, balances, or fees | Avoid opening cards just for bonuses unless you have a clear plan | Missed payments and high balances can damage your credit score |

| How many credit cards should someone have? | It depends on income, spending habits, and financial discipline | Beginners may need one card; experienced users may manage three or more | There is no perfect number for everyone |

| Is it good to have multiple credit cards? | Yes, if used responsibly | Use different cards for cashback, travel, groceries, or emergencies | Multiple cards can increase available credit and improve rewards |

| Is it bad to have multiple credit cards? | Not always | It becomes bad if you overspend, miss payments, or pay unnecessary annual fees | Credit cards are useful tools, but poor management creates debt |

| Is it bad to have too many credit cards? | Yes, if they become difficult to manage | Keep only cards that provide real value | Too many cards can lead to hard inquiries, confusion, fees, and debt risk |

| How many credit cards should one have? | A balanced number is usually 2 to 4 cards for responsible users | Choose cards based on purpose: daily spending, rewards, travel, and backup use | The ideal number should support your financial goals, not complicate them |