Let's Shape The Future Of Your Investments!

Natoque iaculis cursus augue urna commodo aptent morbi tortor porttitor quis ornare.

| Question | Simple Answer |

|---|---|

| Are high limit credit cards good? | Yes, if used responsibly |

| Do high limit cards help credit score? | They can help by lowering credit utilization |

| Is a $5,000 credit card limit good? | Yes, especially for a first strong credit limit |

| Who gets the highest limit credit cards? | People with excellent credit, high income, and low debt |

| Can good credit qualify for high limits? | Yes, but excellent credit gives better chances |

| Should I use the full credit limit? | No, keeping usage low is better for credit health |

Imagine you are planning a dream international vacation for your family, or perhaps you are finally ready to invest in high-end appliances for your home renovation. You go to make the purchase, only to realize that your current credit limit cannot accommodate the transaction. This is where the power of high limit credit cards comes into play.

More than just a financial safety net for massive purchases, cards with substantial credit lines offer a gateway to elevated financial flexibility, premium perks, and even improved credit scores. Whether you are aiming to upgrade your everyday spending capacity or looking to fund a small enterprise, understanding how these financial tools work is essential.

In this comprehensive guide, we will explore the tangible benefits of these cards, how to qualify for them, and actionable strategies for maximizing their potential.

The definition of a “high limit” varies depending on your financial background and credit history. For a college student or someone just establishing their financial footprint, graduating to a 5000 credit card limit can feel like a major milestone. However, in the realm of premium finance, high limits typically start around $10,000 and can easily scale to $50,000, $100,000, or even more.

If you have ever wondered what determines credit card limits, the answer lies in a combination of factors analyzed by the card issuer’s underwriting department. These include:

At the very top of the market are the highest limit credit cards, which are generally reserved for high-net-worth individuals and successful business owners who have proven their ability to manage substantial credit lines responsibly.

When you upgrade to a higher tier of credit, the benefits extend far beyond simply being able to buy more things. In fact, a higher credit limit can actively improve your overall financial health if used strategically.

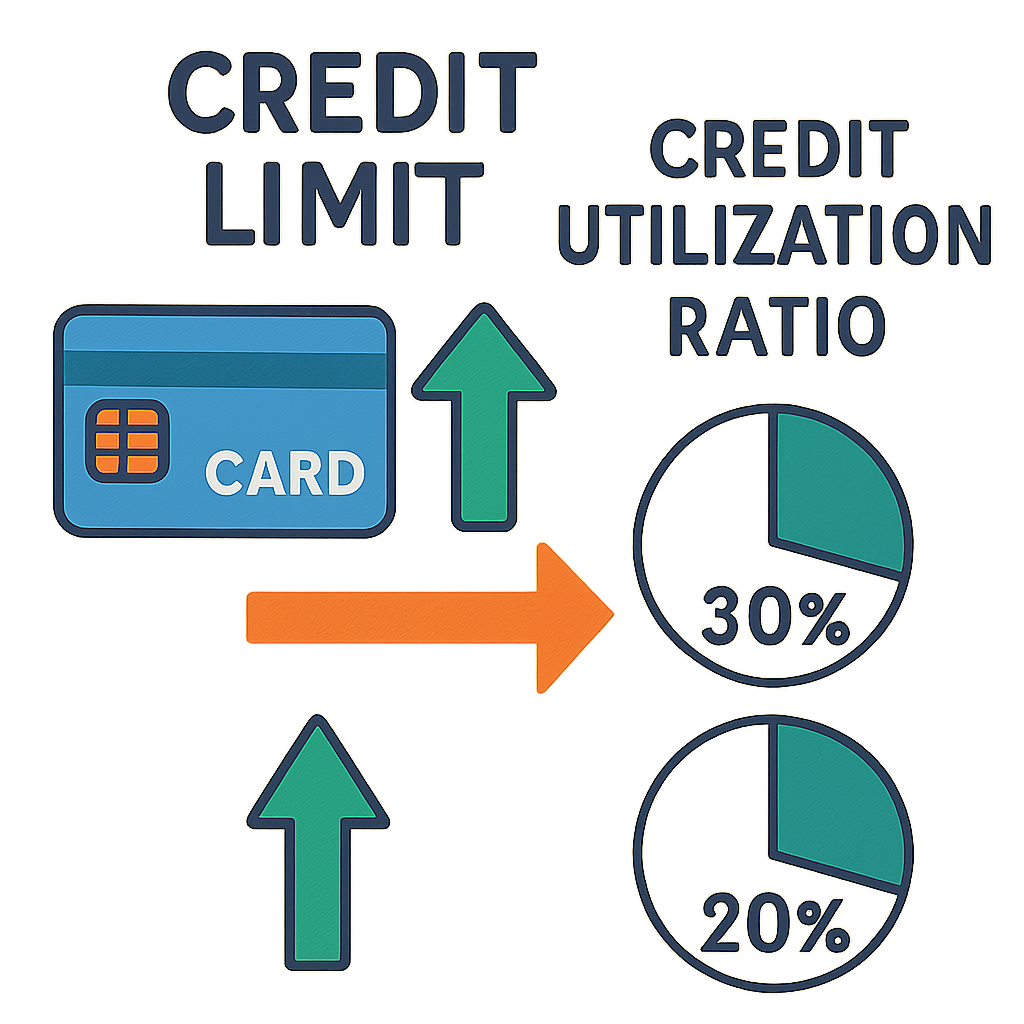

One of the most significant, yet often misunderstood, benefits is lowering credit utilization ratio. Your credit utilization ratio is the amount of revolving credit you are currently using divided by the total amount of credit available to you. It accounts for up to 30% of your FICO score.

For example, if you routinely spend $3,000 a month on a card with a $5,000 limit, your utilization ratio is a very high 60%. This can severely drag down your credit score. However, if you spend that same $3,000 on a card with a $30,000 limit, your utilization drops to just 10%. By maximizing available credit line across your accounts, you can effortlessly maintain a single-digit utilization ratio, which is highly favorable to credit bureaus.

Life is unpredictable. Medical emergencies, sudden home repairs, or emergency travel can cost thousands of dollars. Having a high limit credit card provides immediate liquidity without the need to dip into investment accounts or take out high-interest personal loans.

The difference between top tier vs entry level cards is staggering when you look at the included benefits. Entry-level cards are great for basic cash back or building credit, but high limit cards often belong to the luxury category, offering perks that easily offset their annual fees.

High limit cards are frequently tied to premium travel rewards programs. Cardholders typically enjoy complimentary airport lounge access, accelerated points earning on travel and dining, statement credits for global entry or TSA PreCheck, and elite status with airline and hotel partners.

Additionally, many of these cards offer exclusive concierge services. Whether you need last-minute reservations at a Michelin-starred restaurant, hard-to-get concert tickets, or a tailored travel itinerary, your card’s concierge operates like a personal assistant.

Interestingly, some of the most prestigious cards on the market don’t have a traditional limit at all. Charge cards, for instance, frequently offer no preset spending limit features. Instead of a fixed number, your purchasing power adapts based on your spending habits, income, and payment history. This allows for extraordinary flexibility, provided you pay the balance in full every month.

Securing these highly coveted financial tools requires a solid financial foundation. Issuers are taking on a greater risk by extending large amounts of credit, so their approval criteria are naturally stricter.

The FICO score requirements for luxury cards generally start in the “very good” to “exceptional” range, meaning a score of 740 or higher is typically expected. If you have an immaculate credit history, you should be looking into credit cards for excellent credit high credit limit.

However, if your score is closer to 680 or 700, you are not entirely locked out. There are several high credit limit credit cards for good credit available that can start you off with a respectable $5,000 to $10,000 limit, which can grow over time with responsible use.

Your income is important, but lenders care just as much about your existing obligations. The debt to income ratio for approval plays a pivotal role in the underwriter’s decision. This ratio calculates how much of your monthly income goes toward paying debts. To secure the best high limit credit cards, you generally want a debt-to-income (DTI) ratio below 30%.

For those at the absolute apex of the financial world, qualifying for black cards (like the legendary American Express Centurion Card) is the ultimate goal. These cards are strictly by invitation only. Qualifications are shrouded in secrecy, but they generally require hundreds of thousands of dollars in annual spending across other premium cards, alongside a massive net worth.

If you want to access high limits, you have two primary options: apply for a new premium card, or request an increase on an account you already hold.

When searching for the best high limit credit cards for good credit or excellent credit, look for flagship travel and reward cards from major issuers. Cards categorized as Visa Infinite or World Elite Mastercard typically have minimum credit limits of $5,000 or $10,000 baked into their terms, guaranteeing a high limit upon approval.

You do not always have to open a new account to boost your purchasing power. If you have a good relationship with your current bank, getting an increase is often a streamlined process. Here are some actionable tips on how to increase credit limit instantly:

It is crucial to distinguish between business vs personal spending power. If you are an entrepreneur, freelancer, or small business owner, putting business expenses on a personal high limit card can skew your personal credit utilization and mix personal liability with business debts.

Instead, look into unsecured business lines of credit or high-limit business credit cards. Business cards are evaluated differently, often taking your company’s revenue and time in business into account alongside your personal guarantee. They are designed to handle bulk purchases, inventory orders, and advertising spend, often offering limits vastly superior to personal cards while keeping your personal credit report clean.

With great purchasing power comes great financial responsibility. The overarching danger of a high limit is the temptation of lifestyle inflation.

When managing large revolving balances, the interest charges can compound aggressively. A $20,000 balance at a 20% APR can quickly spiral into a devastating financial burden. To fully enjoy the benefits of high limit cards, strictly adhere to the following rules:

Transitioning to high limit credit cards is a rewarding step in your financial journey. By understanding what determines your limits and carefully curating your credit profile, you can unlock a world of unparalleled purchasing power. Whether you are leveraging these cards for elite travel rewards, lowering your credit utilization, or funding a growing business, the key to success is unwavering financial discipline. Treat your high credit limit as a powerful tool rather than free money, and it will serve you exceptionally well for years to come.

| Keyword Topic | What It Means | Best For | Typical Credit Limit Range | Important Notes |

|---|---|---|---|---|

| High limit credit cards | Credit cards that offer larger spending limits than standard cards | People with strong credit and stable income | Usually $5,000 to $25,000+ | The actual limit depends on credit score, income, debt, and issuer rules |

| Best high limit credit cards | Cards known for offering strong limits and good benefits | Users who want rewards, travel perks, or cashback | $10,000 to $50,000+ | Premium cards often require excellent credit |

| High credit limit credit cards for good credit | Cards available to people with good credit, not necessarily perfect credit | Users with a good credit score and responsible payment history | $5,000 to $15,000+ | Approval is easier than premium cards, but limits may start lower |

| Best high limit credit cards for good credit | Strong card options for users with good credit | Everyday spenders, cashback users, and balance managers | $5,000 to $20,000+ | Good credit may qualify, but income still matters |

| Credit cards for excellent credit high credit limit | Premium cards designed for top credit profiles | High-income earners, business owners, frequent travelers | $15,000 to $100,000+ | Excellent credit improves approval chances but does not guarantee a high limit |

| Highest limit credit cards | Cards that may offer very large credit limits | Experienced borrowers and premium cardholders | $25,000 to $100,000+ | Some charge cards may not have a preset spending limit |

| 5000 credit card limit | A card with a $5,000 credit limit | Beginners moving into stronger credit products | Around $5,000 | A $5,000 limit is often considered a solid starting high limit for many users |