Let's Shape The Future Of Your Investments!

Natoque iaculis cursus augue urna commodo aptent morbi tortor porttitor quis ornare.

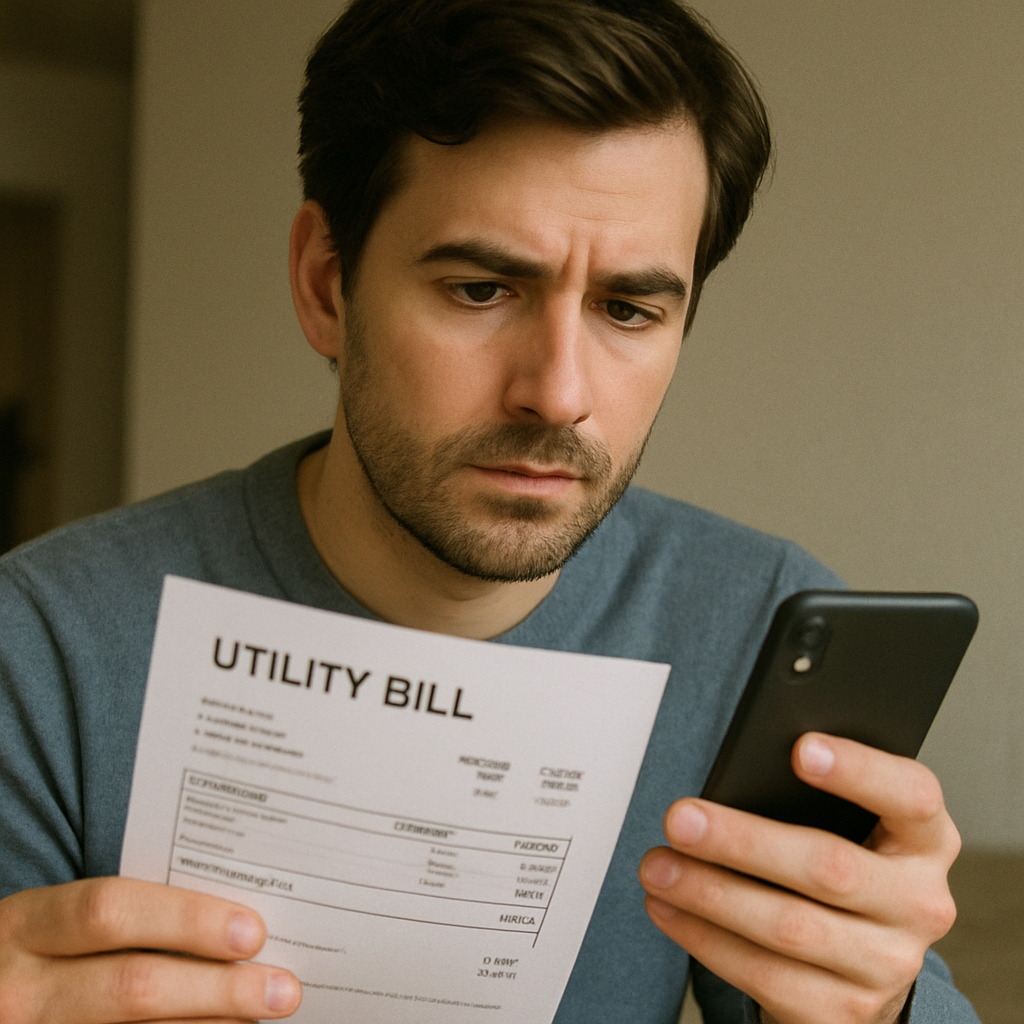

It is three days until payday, and an unexpectedly high utility bill just dropped into your mailbox. Your immediate thought is, “I need 200 dollars now,” but acting on pure panic can make a tight situation much worse. According to consumer financial advocates, the “easiest” emergency cash is often the most expensive. We need a prioritization strategy that fixes today’s problem without creating a new one next week.

How do you balance getting money fast against paying unfair fees? Every time you borrow 200 dollars, you face a critical speed-versus-cost tradeoff. To protect yourself, we will use the “Wallet Impact” strategy. This simple approach means looking past confusing banking terms and asking exactly how much extra cash a lender will physically remove from your next paycheck.

Safe options exist to secure a 200 dollar loan, even if your credit score is less than perfect. This guide serves as your roadmap to finding the quickest cash at the lowest cost. By understanding these choices upfront, you handle the emergency confidently while keeping your future finances secure.

When a utility bill is unexpectedly high, you just need a quick solution to avoid late fees. Today, getting money fast means choosing between smartphone apps and storefront lenders. Understanding the difference between cash advance apps vs payday loans can easily save you forty dollars or more out of your very next paycheck.

Instead of charging interest, modern financial technology (fintech) apps use a tip-based model. They ask for an optional “tip” or a small monthly subscription rather than a massive mandatory fee. Here is the typical cost to borrow $200 across different options:

Those numbers clearly prove why a 200 payday loan should always be your absolute last resort. Traditional lenders trap you with huge, unavoidable fees that make it incredibly hard to afford basic groceries when your actual payday finally arrives.

Before applying for 200 loans payday advance, you must know exactly how much “renting” this cash removes from your pocket. Making a safe choice means looking past clever advertising to calculate the true wallet impact.

Paying thirty dollars to borrow cash for a flat tire seems harmless in a stressful emergency. Yet, that flat fee completely masks the true wallet impact of a 200 dollar loan. If you rent that money for just two weeks and are required to pay back $230, you are actually paying a massive premium for a very short timeframe.

Financial experts expose this hidden expense using a “yearly yardstick” called APR (Annual Percentage Rate). This measurement calculates what your short-term cash rent would cost if you kept the money for an entire year. Applying this yardstick turns a simple $30 fee into a staggering APR near 400%, quickly proving why standard interest rates for small personal credit lines are significantly safer than storefront payday traps.

Fortunately, the law provides a built-in safety net so you never have to guess these steep numbers. Under truth in lending act disclosure requirements, every lender must clearly state the APR and the exact total dollar cost before you sign anything. Knowing your actual cost is crucial, but you also need to protect your financial footprint.

Every time you apply for funding, a lender leaves a footprint on your credit report. A “hard” pull leaves a deep track that temporarily lowers your score, making any search for a 200 loan bad credit solution much more stressful. Fortunately, modern services use a “soft” pull instead. This light footprint lets the lender verify your identity without damaging your score at all.

Figuring out how to get quick money without a credit check means leveraging your actual bank history instead of a three-digit number. Many lenders simply review your regular paycheck deposits to grant approval. Before applying anywhere, always look for a clear guarantee on their website stating that checking your rate will not affect your score.

When you need safe cash fast, consider these common no hard credit pull lending options:

Keeping that footprint light ensures your financial foundation stays strong while you handle unexpected emergencies. Sometimes, the safest route skips new applications entirely.

Sometimes the quickest emergency cash is already inside your bank account. When a $200 bill hits a zero balance, choosing overdraft protection vs small installment borrowing might save you money. A $35 bank overdraft fee is a single, flat cost. This briefly borrows from your next paycheck without trapping you in the endless weekly fees of predatory lenders.

Moving your banking to a local branch unlocks a safer credit union alternative to high interest lenders. They offer Payday Alternative Loans (PALs), which cap the cost of renting money at a 28% APR—meaning a $200 loan costs mere dollars in interest, not $50. Use this simple checklist for improving eligibility for short term financing:

Building these relationships creates a strong financial safety net for tomorrow. But if you need money for an immediate emergency right now, the clock is ticking.

When you need to get 200 dollars now, every minute counts. Securing a same day funding direct deposit means applying before the lender’s daily cut-off time, which is usually noon. Missing this early window automatically pushes your cash to the next business day. You can prevent frustrating holdups by having your driver’s license and a recent pay stub ready before you even start the application.

How lenders actually send the money matters just as much as when you apply. Standard “ACH transfers” move funds through the regular banking system slowly, often taking one to three days to clear. To ensure fast funding for minor financial gaps, select “Instant Debit funding” instead. This modern method pushes the cash directly to your debit card within minutes, though lenders typically charge a small extra fee for the speed.

Rushing to find immediate relief can unfortunately make you a target for bad actors. Before accepting the first rapid offer you see, you must learn to identify dangerous terms.

When covering unexpected bills with short term credit, stress can make dangerous offers look like lifesavers. Predatory lending happens when companies use unfair terms to drain your future paychecks. If you just need to borrow 200 dollars, you must protect your bank account from these debt traps.

Watch out for these predatory lending signs to avoid:

Reading the fine print stops a small gap from becoming a massive hole. Once you secure safe funding, you need a quick exit strategy.

You no longer have to panic and wonder where can I borrow a small amount of money today without getting trapped by hidden fees. You now have the exact tools needed to safely secure a small cash advance for emergencies. Start tonight by comparing a reputable cash app against your local credit union to find the lowest fee.

Before accepting any funds, carefully review the repayment terms for emergency cash advances to ensure your total borrowing cost stays under $15. Calculate the precise wallet impact this deduction will have on your next paycheck so you can budget accordingly and completely avoid late penalties.

Handling a sudden financial curveball shouldn’t create a deeper hole next month. Once this immediate stress is cleared, try directing just five dollars a week into a mini-emergency fund, transforming today’s urgent hurdle into a foundation for future financial peace of mind.