Let's Shape The Future Of Your Investments!

Natoque iaculis cursus augue urna commodo aptent morbi tortor porttitor quis ornare.

Most of us cannot pull the full cost of a college degree out of a literal pocketbook. When looking at your financial aid package, you might wonder exactly what are student loans compared to scholarships. Unlike a grant, which is free money, a loan acts as a financial bridge to your future career—but it is money with a long memory.

At its core, the student loan meaning comes down to a simple exchange: borrowing cash today using tomorrow’s expected earning power. Once approved, you receive the principal to cover immediate expenses like tuition, fees, or textbooks.

In practice, according to the Department of Education, securing these funds requires signing a Master Promissory Note. Think of this document as the ultimate “I.O.U.” that establishes a strict legal obligation to repay the debt, even if you do not finish your degree or find a job immediately.

Viewing this debt as a powerful investment tool helps you borrow carefully and make smarter choices before classes even start.

Defining student loan obligations requires looking beyond the initial handshake and exploring the math underneath. The mechanics of student loans always start with the principal—the original, exact amount you borrowed to cover tuition, textbooks, or a dorm room. For instance, if you take out $10,000 to pay for your freshman year, that flat ten grand is your starting principal.

Money, however, is rarely lent for free. Think of interest as the “rent” you pay to a bank or the government for the privilege of using their money to get your degree. Depending on the interest rate types for student debt you agree to, this rent is charged as a steady percentage of your principal. Every month you hold onto their money, a new rent charge is added to your balance, meaning the debt slowly grows over time.

Ultimately, combining your initial principal with all that accumulated rent creates your total cost of borrowing. Calculating total cost of borrowing reveals why the final price tag of your degree is always higher than the original sticker price. Knowing exactly how this debt grows prepares you perfectly for choosing your lending partner.

When deciding how to fund your education, you are essentially choosing between two financial paths: the U.S. government or a private bank. Weighing federal vs private student loans dictates not just who you owe, but how safely you can repay them in the future.

Three major dividing lines separate private student loans from government options:

Since most students lack a long financial track record, banks view them as risky investments. Therefore, they enforce strict cosigner requirements for private loans. A cosigner is a parent or trusted adult who legally promises to pay the debt if you cannot, meaning a single missed payment damages both of your credit scores simultaneously.

Relying on the government route is generally the safest starting point for most families. However, even within that protective federal umbrella, not all borrowed money behaves identically while you sit in class.

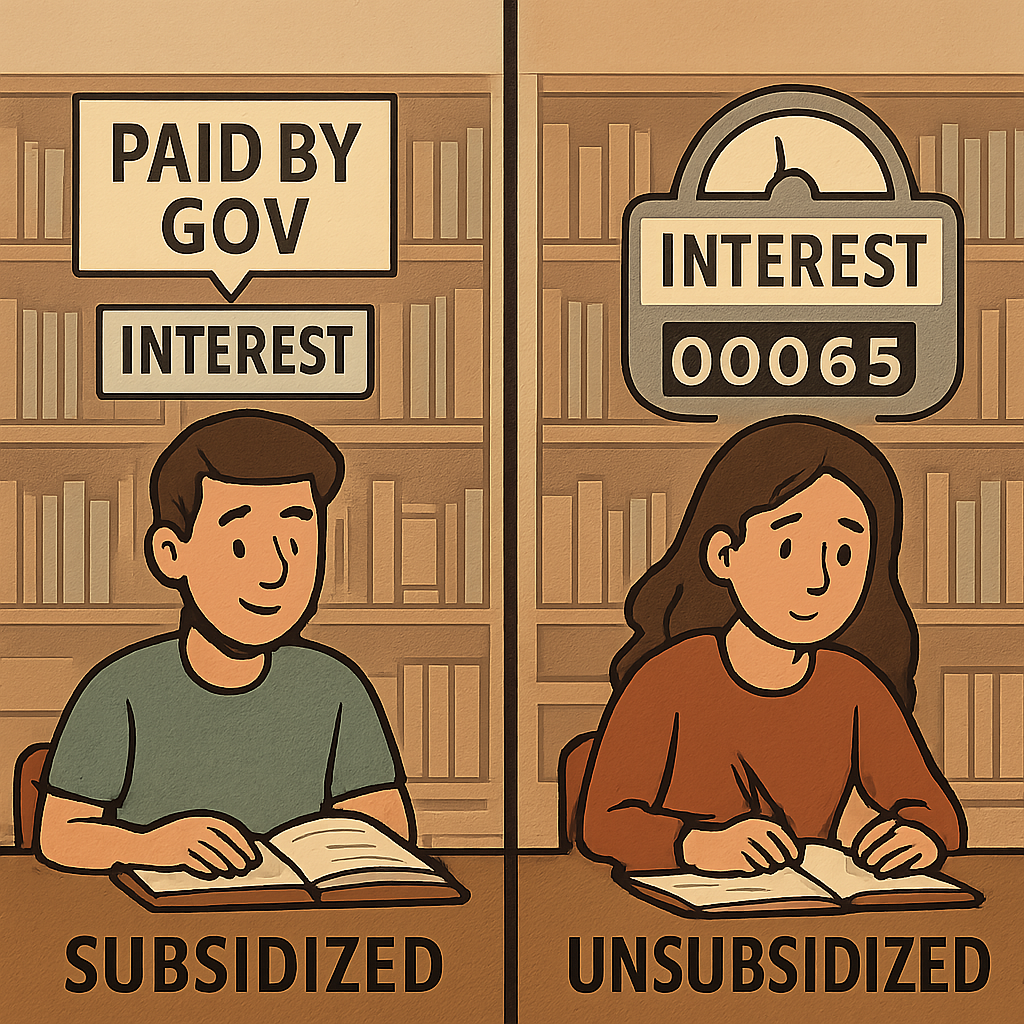

Imagine moving into an apartment where the landlord charges rent, but delays the bill until years later—that is how interest works on most college debt. When comparing direct subsidized vs unsubsidized loans, the key difference is who pays that “rent” while you study. If you receive an unsubsidized loan, the interest meter starts running immediately. This process—known as interest accrual—means your balance grows quietly in the background while you sit in a lecture hall.

By contrast, the government acts as a financial shield if you qualify for a subsidized version. They completely cover your interest charges while you are enrolled in classes, meaning a $5,000 loan remains exactly $5,000 on graduation day. This subsidy provides a massive cost-saving benefit, protecting you from facing a much larger balance than you originally borrowed when you enter the workforce.

Securing this better deal depends entirely on proving financial need during the FAFSA application process. Your submitted family information dictates whether the government grants you this vital interest protection. Just remember that unlike grants—which are free money—both of these borrowing paths eventually require monthly payments.

Securing college funding is a multi-year journey that begins long before campus life. It kicks off with the FAFSA application process to determine your federal aid eligibility. If you borrow, reviewing the master promissory note definition—the binding legal contract where you promise to repay the debt—is your first true step into the borrowing lifecycle.

Following that signature, your funds travel through four predictable milestones:

Navigating this transition requires knowing the middleman assigned to your account. Handling your billing and processing payments fall under core student loan servicer responsibilities. Because this company collects your money when the six-month window closes, engaging with them early protects your credit score from accidental missed payments.

Leaving school often sparks exciting goals like buying a reliable car or a first home. However, lenders closely examine your debt-to-income ratio—a simple comparison of how much you earn versus what you owe monthly—before approving new applications. The impact of student loans on credit is significant because a high monthly bill can make you appear risky to a mortgage or auto lender, though paying that bill responsibly builds an excellent credit history over time.

When juggling multiple accounts becomes overwhelming, student loan consolidation and refinancing offer distinct ways to simplify your repayment. Consolidation bundles your federal loans into one monthly payment while keeping them safely inside the government system. Refinancing means transferring your debt to a private bank to potentially secure a lower interest rate, which unfortunately permanently erases your federal safety nets.

Teachers, nurses, and government workers have a unique advantage if they keep their debt federal. By utilizing specific income-based student loan repayment options, these professionals can eventually erase their remaining balances. The core public service loan forgiveness requirements involve working full-time for a qualifying non-profit or government employer while making exactly 120 on-time monthly payments.

Mastering these long-term financial levers removes the intimidation factor from borrowing. Knowing how monthly obligations shape your purchasing power, strategically combining debts, and targeting forgiveness programs ensures your degree supports your future rather than restricting it.

These financial tools are simply a bridge to your future career. Evaluating your award letters by identifying the exact “rent” you will pay on borrowed money positions you to make sound financial decisions.

Your immediate next step is applying a golden rule of borrowing: never take out more than you expect to earn in your first year after graduation. Before accepting any offer, plug those total numbers into an online loan calculator to preview your future monthly bill.

Borrowing only what is strictly necessary protects your post-graduation lifestyle. Each time you estimate your payments ahead of time, you build the confidence needed to cross that bridge and start your career on solid ground.