Let's Shape The Future Of Your Investments!

Natoque iaculis cursus augue urna commodo aptent morbi tortor porttitor quis ornare.

Navigating the world of mortgages can be daunting. The language used is often complex and filled with jargon. Understanding mortgage terms is crucial for making informed decisions.

Whether you’re a first-time homebuyer or considering refinancing, knowing these terms can save you money. It can also help you avoid costly mistakes.

Mortgages are not just about interest rates and monthly payments. They involve various terms that impact your financial future.

This guide will break down common mortgage terms. It aims to empower you with the knowledge needed to navigate the mortgage process confidently.

Let’s dive into the essential terms you need to know.

Grasping the ins and outs of mortgage terms is vital. It not only helps you understand what you’re signing but also gives you an edge in negotiations. Without this knowledge, important details can be easily overlooked.

Knowing key terms can improve your financial decision-making. It ensures you are prepared and confident at every step of the process. You’ll be less likely to encounter unwelcome surprises.

Consider the following reasons why understanding these terms is essential:

Informed borrowers tend to make wiser choices, leading to long-term benefits.

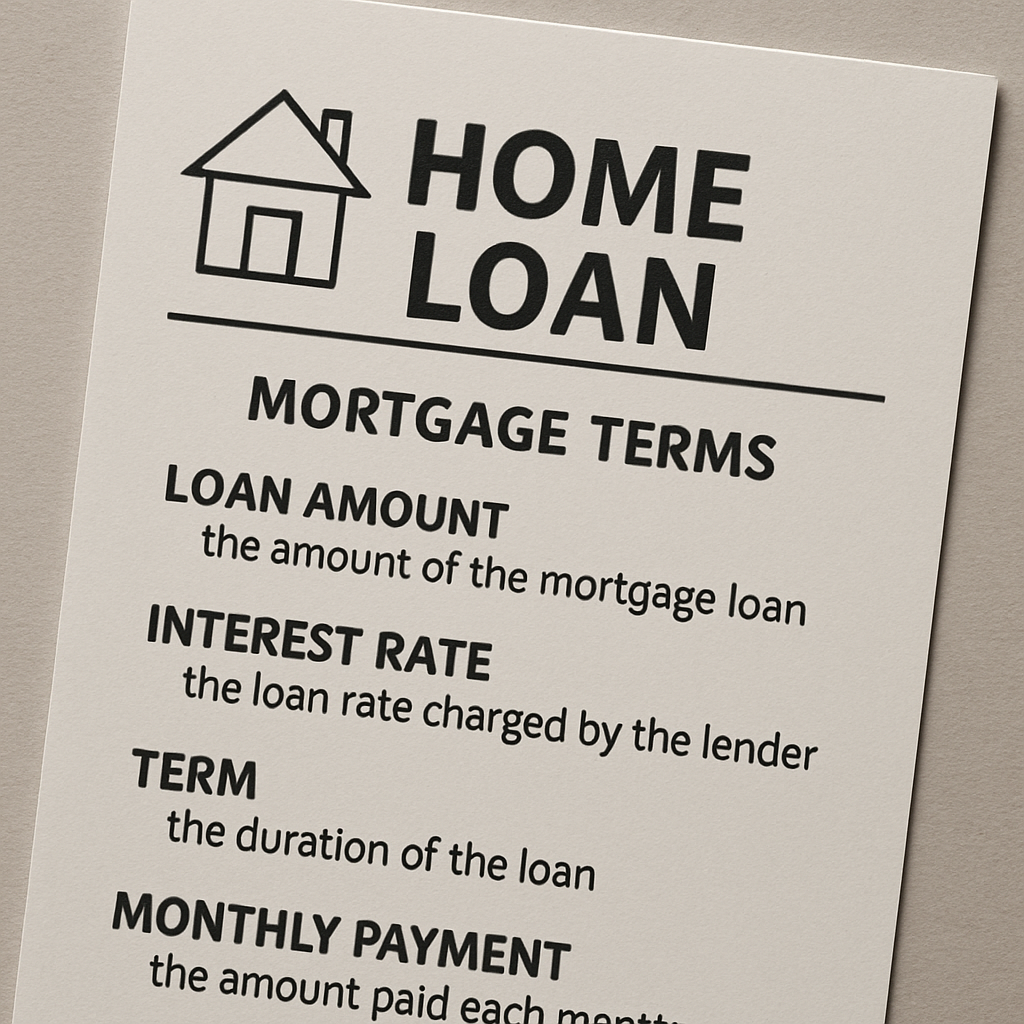

Understanding mortgage loan terms is crucial when buying a home. Let’s break down some common terms you will encounter. This will prepare you for informed discussions with lenders.

Principal is the initial amount you borrow to purchase your home. It excludes interest, which is separately calculated. The principal decreases as you make payments.

Interest is the cost of borrowing money from a lender. It is usually expressed as a percentage of the principal. Lower interest rates make a loan less expensive overall.

The loan term is the period over which you agree to repay the loan. Common terms are 15 years or 30 years, but other options may be available. The length of the term affects monthly payments and the total interest paid.

A fixed-rate mortgage maintains the same interest rate over the loan’s life. This stability helps with budget planning. Your payments remain constant, unaffected by market changes.

An adjustable-rate mortgage (ARM) has an interest rate that can change after an initial period. The rate varies based on market conditions. Initial payments might be lower, but future rates are unpredictable.

Amortization is the process of spreading loan payments over time. Each payment applies to both principal and interest. An amortization schedule shows this breakdown, helping track how much you owe.

Private Mortgage Insurance (PMI) is necessary if your down payment is less than 20% of the home price. It protects the lender if you default on the loan. However, with enough equity, PMI is no longer required.

The equity in your home is the difference between its market value and your outstanding mortgage balance. As you make payments, equity increases over time, strengthening your financial position.

Finally, closing costs include various fees paid upon finalizing the home purchase. These cover services like appraisals, title insurance, and more. Plan for these expenses to avoid surprises at the closing table.

These key terms guide you in understanding mortgage basics. Educating yourself on these can lead to smarter decisions and a smoother homebuying journey.

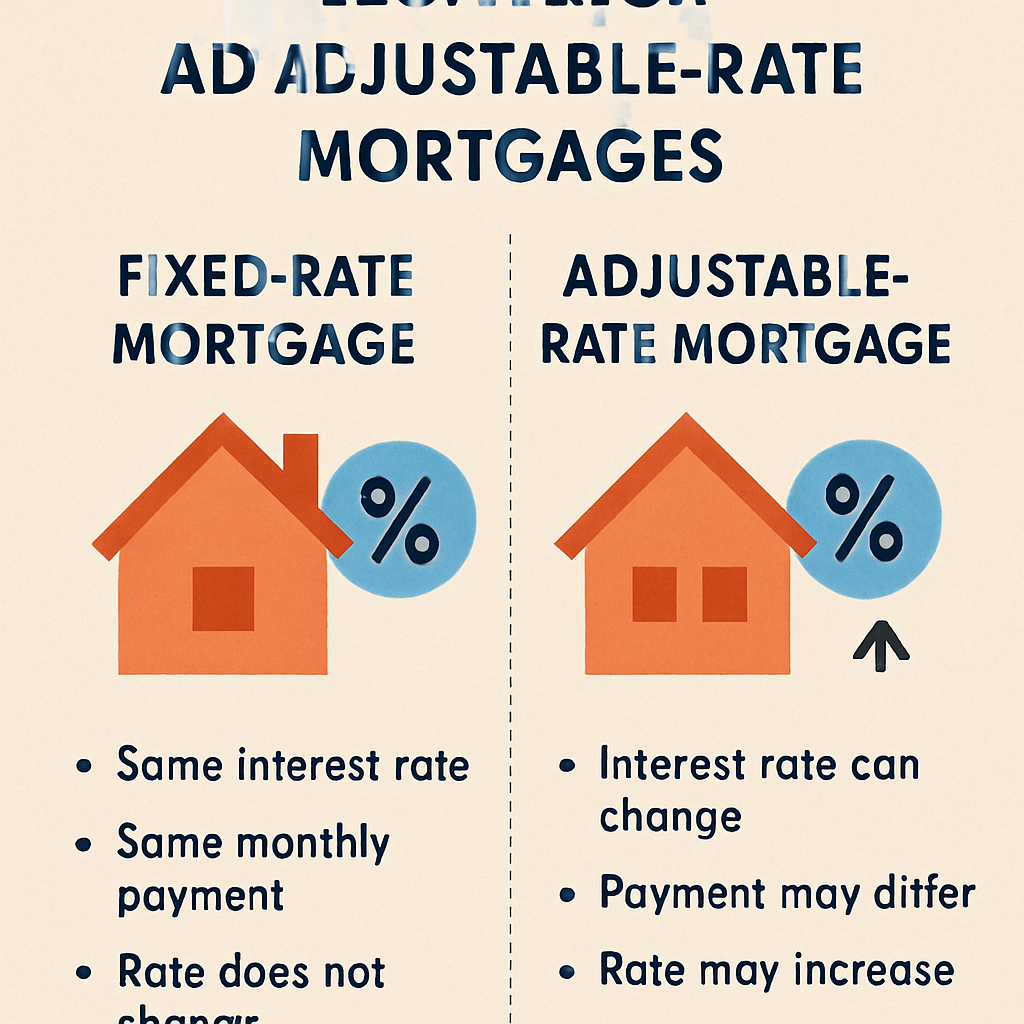

Choosing between a fixed-rate and an adjustable-rate mortgage (ARM) is a key decision. Each has advantages and potential downsides. Understanding them helps you choose the right loan for your situation.

A fixed-rate mortgage guarantees stable payments for the loan’s life. The interest rate stays unchanged, offering predictability. This makes budgeting easier as you’ll always know your monthly payment amount.

In contrast, an adjustable-rate mortgage (ARM) offers initially lower rates. After an initial period, the rate adjusts based on market trends. This can lead to lower payments initially, but future increases are possible.

Consider the following when comparing these mortgage types:

Ultimately, your choice depends on your financial plans and comfort with potential rate changes. Carefully assess your long-term goals and risk tolerance before deciding.

Refinancing involves replacing an existing home loan with a new one. It’s often done to secure better terms or a lower interest rate. Here are key terms you’ll encounter during this process.

Interest Rate is pivotal when refinancing. Even a small difference can lead to significant savings over the loan’s term. Be sure to compare rates from various lenders before deciding.

The closing costs in refinancing can impact overall savings. These fees cover various services like appraisals, title insurance, and attorney fees. Understand them fully to gauge the real cost of refinancing.

Loan-to-value (LTV) ratio is another critical factor. It compares your loan amount to your home’s current value. A lower LTV can improve your chances of approval and better terms.

Consider these terms when exploring refinancing options:

Exploring these options can provide financial flexibility. A well-informed choice can lead to long-term savings and improved loan conditions.

Reverse mortgages offer a financial solution for older homeowners. This loan allows conversion of home equity into cash, without selling the property. Key terms help you navigate this option.

A Home Equity Conversion Mortgage (HECM) is the most common reverse mortgage. It’s insured by the FHA, providing security for both borrowers and lenders.

With a reverse mortgage, there is no need for monthly payments. Instead, the loan balance grows over time, repaid when the home is sold or the homeowner passes away.

Understand these essential reverse mortgage terms:

by Vitaly Gariev (https://unsplash.com/@silverkblack)

Examining these terms can clarify reverse mortgage decisions, offering peace of mind and financial independence.

Navigating the mortgage industry requires familiarity with various terms and acronyms. These can seem daunting but are essential for making informed choices.

One crucial term is the Annual Percentage Rate (APR). This figure represents the total cost of borrowing, including interest and fees, expressed as a yearly rate.

The Debt-to-Income (DTI) Ratio indicates a borrower’s financial health. It compares monthly debt payments to gross income, influencing loan approval decisions.

Familiarize yourself with common mortgage industry acronyms:

Understanding these terms equips you to confidently engage with lenders and brokers. With this knowledge, you can better manage your mortgage journey and potentially secure favorable terms.

When securing a mortgage, it’s essential to understand the associated fees and costs. These can significantly affect the total cost of homeownership.

Closing costs are a major component and can include several fees. They generally range from 2% to 5% of the loan amount. These costs cover various services needed to finalize the mortgage.

There’s also the origination fee, a charge by the lender for processing your loan application. This fee is typically around 1% of the loan and can sometimes be negotiated.

Another key element is Private Mortgage Insurance (PMI), often required if your down payment is less than 20%. PMI protects the lender and adds to your monthly costs.

Here’s a list of common mortgage fees:

Negotiating some of these costs can lead to savings. Always ask your lender for a detailed cost breakdown before closing.

by Jakub Żerdzicki (https://unsplash.com/@jakubzerdzicki)

Navigating mortgage documents can feel overwhelming. It’s critical to understand every detail before signing anything. This ensures you’re fully aware of your commitments.

Start by reviewing the Good Faith Estimate (GFE). This gives a heads-up on potential costs. Understanding this can prevent surprises at closing.

The Truth in Lending Act (TILA) disclosure is another essential document. It explains the total cost of your loan, including interest and fees, in simple terms.

Here are some tips to help you navigate these documents:

Being proactive and attentive can save you from costly mistakes. Don’t hesitate to seek professional advice if necessary.

Understanding mortgage terms can be challenging. Many people have questions about this complex area. Answers to common questions can shed light on your uncertainties.

What is a fixed-rate mortgage? This is a mortgage with an interest rate that stays the same throughout the loan’s term. It provides predictable monthly payments.

What’s the difference between a pre-approval and pre-qualification? Pre-approval involves a more thorough check of finances and gives a more reliable borrowing limit than pre-qualification, which is less rigorous.

To clarify additional doubts, consider the following:

Having answers to these FAQs helps in making well-informed mortgage decisions. Always seek expert advice if needed, to ensure clarity on your mortgage journey.

Understanding mortgage terms empowers you during home-buying or refinancing. Knowing key terms helps you make informed decisions about your mortgage options. This knowledge can save you money and prevent costly mistakes.

Remember to review documents and disclosures carefully. Comprehending your loan’s specifics is crucial to managing finances effectively. Equipped with this knowledge, you’ll be better positioned to negotiate terms that best suit your needs.

If you’re ever unsure, don’t hesitate to seek professional advice. Mortgage professionals can guide you through complex details, ensuring clarity and confidence in your decisions. Being well-informed is your best tool in navigating the mortgage landscape.