Let's Shape The Future Of Your Investments!

Natoque iaculis cursus augue urna commodo aptent morbi tortor porttitor quis ornare.

Buying a home is one of the most exciting financial milestones you can achieve, but the process of financing that purchase can easily feel overwhelming. If you are stepping into the real estate market for the first time, you are likely asking yourself: exactly how do mortgages work?

Whether you are just starting to browse real estate listings or you are preparing to make an offer, understanding the mechanics of home loans will empower you to make smarter financial decisions. In this comprehensive guide, we will break down the terminology, explore the lending process, and give you the knowledge you need to navigate the housing market with confidence.

Before diving into complex interest rates and loan structures, let’s start at the very beginning. If you ask a financial expert to define mortgage, they will tell you that it is a legally binding agreement between a borrower and a lender to purchase real estate.

To explore the mortgage meaning more deeply, it is essentially a secured loan. When you borrow money to buy a house, you sign an agreement stating that you will pay back the loan over a set period, plus interest. The most crucial part of the mortgage definition is that the property itself serves as collateral. If you stop making your payments, the lender has the right to take possession of the property through a process known as foreclosure.

For a quick mortgage def, just think of it as a “pledge.” In fact, the word stems from a French law term meaning “dead pledge”—meaning the pledge dies when the debt is fully paid or when payment fails.

So, what is a mortgage in everyday practical terms? It is the financial vehicle that allows you to buy a home today and pay for it over the next several decades.

If you are wondering, how does mortgage work on a practical level, the concept is quite straightforward. Because houses are expensive, very few people have the cash to buy them outright.

Instead, you provide a portion of the home’s purchase price upfront (your down payment), and a bank or lender covers the rest. You then repay the lender in monthly installments over a predetermined number of years—usually 15 to 30 years.

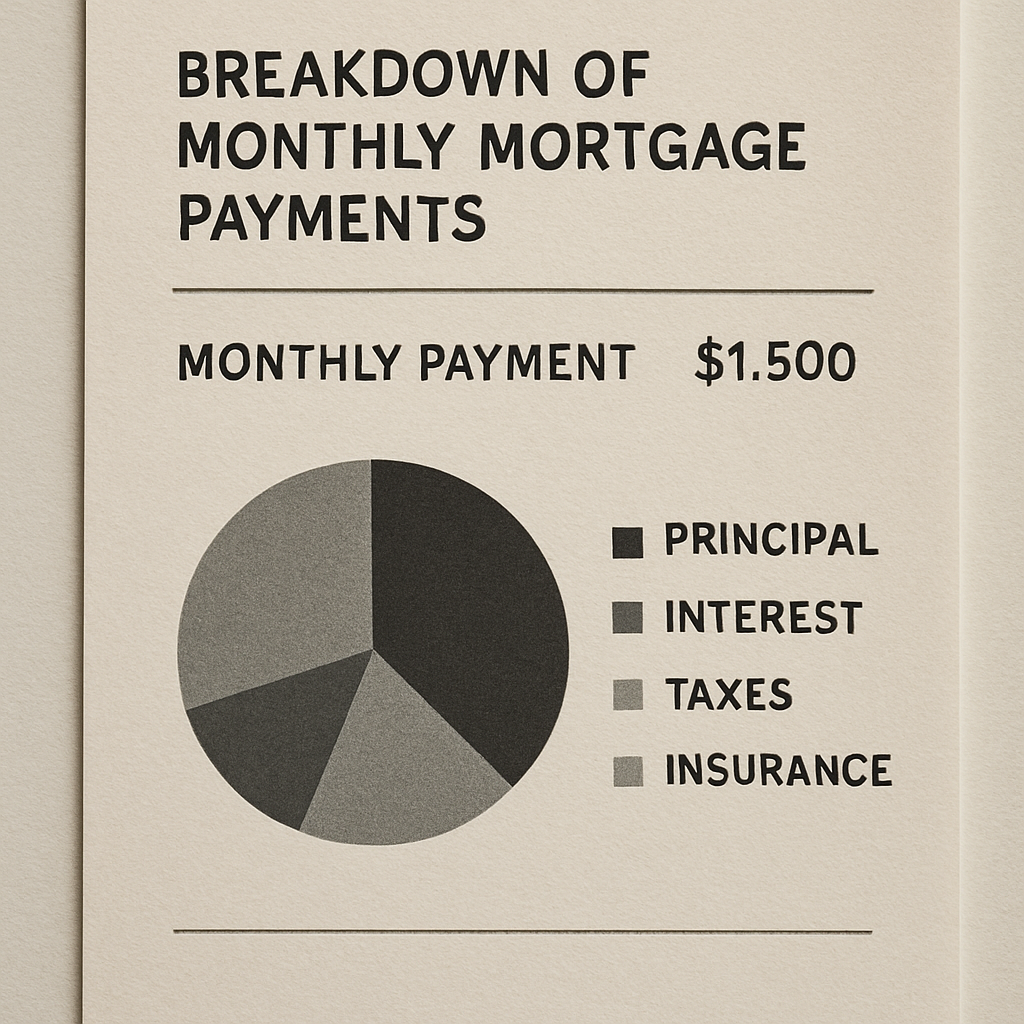

But when people ask how do mortgages work over the long haul, they are usually curious about what exactly makes up that monthly bill. Your monthly mortgage payment is not just a single charge; it is actually a combination of several different financial elements.

Your monthly payment is typically made up of four main parts, commonly referred to as PITI (Principal, Interest, Taxes, and Insurance):

Additionally, understanding private mortgage insurance (PMI) is vital if you are putting down less than 20% of the home’s purchase price. PMI protects the lender—not you—in case you default on the loan. It is an extra monthly fee added to your mortgage payment, though it can usually be canceled once you build up 20% equity in the home.

One of the biggest surprises for new homeowners is seeing how their payments are applied over time. This is where having the mortgage amortization schedule explained becomes incredibly helpful.

Amortization is the process of spreading out your loan into a series of fixed payments. Even though your total monthly payment (principal + interest) remains the same on a fixed-rate loan, the ratio of what you are paying changes dramatically over the life of the loan.

In the first few years, the vast majority of your monthly payment goes toward paying off the interest, with only a tiny fraction reducing the principal balance. As the years go by, this ratio shifts. By the final years of your loan, most of your payment goes directly toward the principal.

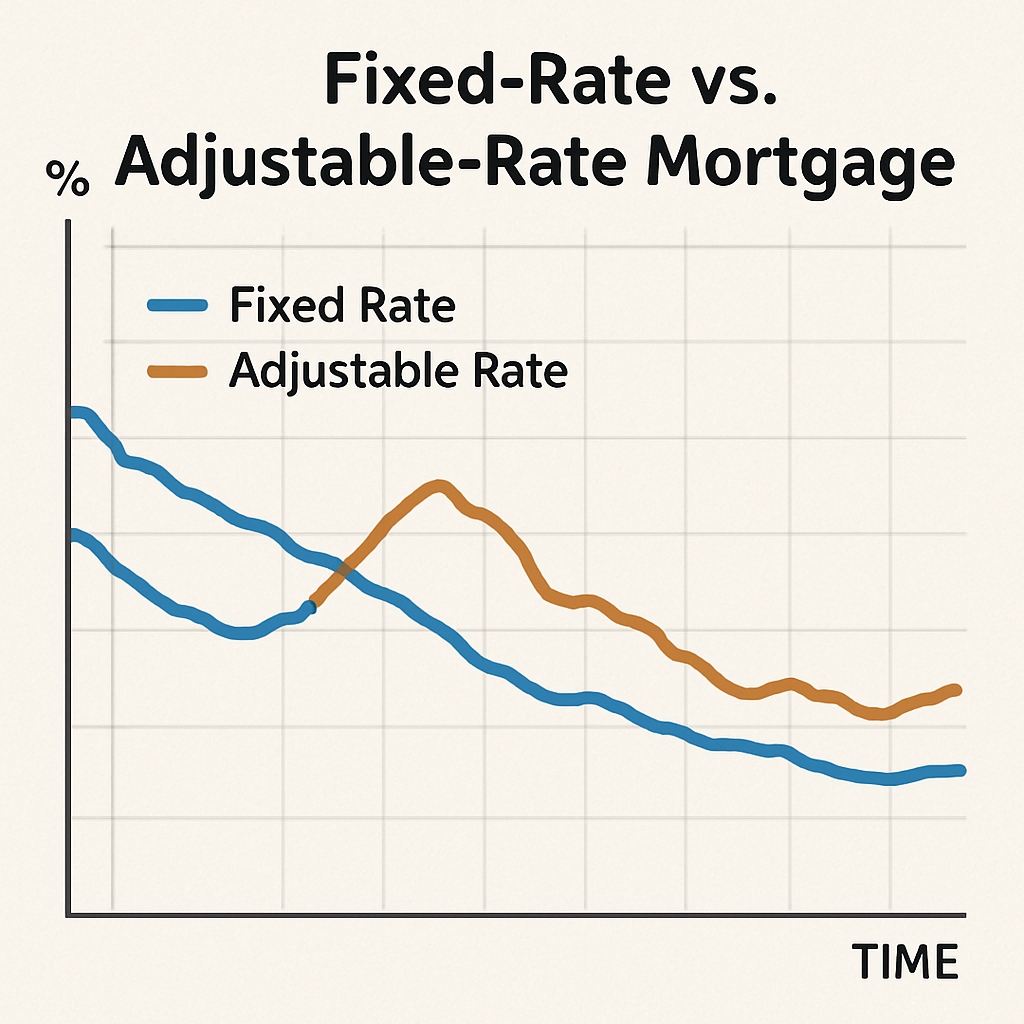

Not all mortgages are created equal. Depending on your financial situation, you will need to choose the loan structure and term that best fits your lifestyle.

When comparing fixed-rate vs adjustable-rate mortgages (ARMs), you are looking at two very different strategies.

You will also need to decide on the type of loan program you want to use. Navigating conventional vs fha loan requirements is a common crossroads for buyers.

The standard mortgage term is 30 years, giving you lower monthly payments. However, the benefits of a 15-year mortgage term are massive for those who can afford a higher monthly payment. With a 15-year loan, you secure a significantly lower interest rate and pay tens (or hundreds) of thousands of dollars less in total interest over the life of the loan. You also build home equity twice as fast.

Securing a mortgage is a multi-step journey. Before you start touring open houses, you need to get your finances in order and prove your reliability to lenders.

Many buyers confuse these two terms, but the difference between pre-qualified and pre-approved is substantial.

The mortgage pre-approval process steps typically involve:

Two major factors dictate your borrowing power: your credit score and your debt-to-income (DTI) ratio.

The impact of credit score on interest rates cannot be overstated. Lenders use your credit score to gauge your risk level. A higher score (typically 740+) unlocks the lowest available interest rates, while lower scores will saddle you with higher rates, meaning a more expensive monthly payment.

Next, lenders will look at how to calculate debt-to-income ratio. This ratio compares your gross monthly income to your total monthly debt payments (including car loans, student loans, minimum credit card payments, and your projected new mortgage). To calculate it, divide your total monthly debt by your gross monthly income, then multiply by 100 to get a percentage. Lenders generally want to see a DTI of 43% or lower, though 36% is considered ideal.

Actionable Tip: Ways to Lower Mortgage Interest Rates If you want to secure the best possible deal, consider these ways to lower mortgage interest rates:

Once you have an accepted offer on a house, your loan moves into the final stages.

First, your file goes to a loan underwriter. The home loan underwriting process stages include an initial review of your updated finances, ordering a home appraisal to ensure the house is worth the purchase price, and issuing “conditional approval.” The underwriter may ask you for a letter explaining a large bank deposit or request a missing document. Once all conditions are met, you receive the highly coveted “Clear to Close” status.

During this time, you will also learn about the role of escrow in home buying. Escrow is a legal arrangement where a neutral third party holds funds and important documents until all the conditions of the real estate sale are met. This protects both the buyer and the seller, ensuring no money changes hands until the title is clear and the contract is fulfilled.

Finally, you will attend closing. The closing table is where you sign the final paperwork and pay your closing costs. A standard mortgage closing costs breakdown typically ranges from 2% to 5% of the loan amount and includes:

You have signed the papers, received the keys, and moved into your new home. But the mortgage process has one final behind-the-scenes step.

Many borrowers are surprised when they receive a letter a few months later stating that their loan has been sold. This introduces you to the secondary mortgage market and loan servicing.

Banks and lenders frequently sell their mortgages to government-sponsored enterprises like Fannie Mae or Freddie Mac, or to private investors on the secondary market. This frees up the lender’s capital so they can go out and fund more loans for other home buyers.

Even if your loan is sold, the terms of your mortgage will not change. However, the company that collects your payments and manages your escrow account—known as your loan servicer—might change. It is completely normal and simply part of how the global real estate economy functions.

Understanding how mortgages work doesn’t require a degree in finance. By learning the difference between pre-qualification and pre-approval, understanding how to manage your credit and DTI, and grasping the breakdown of your monthly payments, you remove the mystery from the home-buying process.

A mortgage is ultimately a powerful tool that, when managed wisely, opens the door to building generational wealth and achieving the dream of homeownership. Take the time to evaluate your finances, shop around for the best rates, and choose a loan that fits your long-term goals. Welcome home!