Let's Shape The Future Of Your Investments!

Natoque iaculis cursus augue urna commodo aptent morbi tortor porttitor quis ornare.

Navigating the mortgage process can feel like learning an entirely new language. Between escrow accounts, amortization schedules, and varying interest rates, the sheer volume of financial jargon is enough to make anyone’s head spin.

One of the most common stumbling blocks for homebuyers and refinancers alike is the concept of “points.” If you are sitting at your kitchen table, staring at a stack of loan estimates and asking yourself, “in terms of a loan what is a point?”, you are certainly not alone. Understanding this single financial concept can be the difference between overpaying for your home and saving thousands of dollars over the life of your mortgage.

In this comprehensive guide, we will break down exactly how this mechanism works, how it affects your wallet, and whether you should utilize it for your next real estate transaction.

To kick things off, let’s address the most fundamental question: what are mortgage points?

Simply put, points are fees you pay directly to your lender at closing. But what is a point in terms of a loan mathematically? The formula is remarkably straightforward. Regardless of the size of your mortgage, one point is always equal to exactly one percent of loan amount.

For example, if you are borrowing $300,000 to purchase a new home, one point equals $3,000. If you are taking out a $500,000 mortgage, one point equals $5,000.

When people search online for “in terms of loan what is a point,” they are usually trying to figure out why they are being asked to pay this large lump sum upfront. The answer lies in how these points function as a financial tool. When you pay these points, you are essentially making a trade-off with the lender.

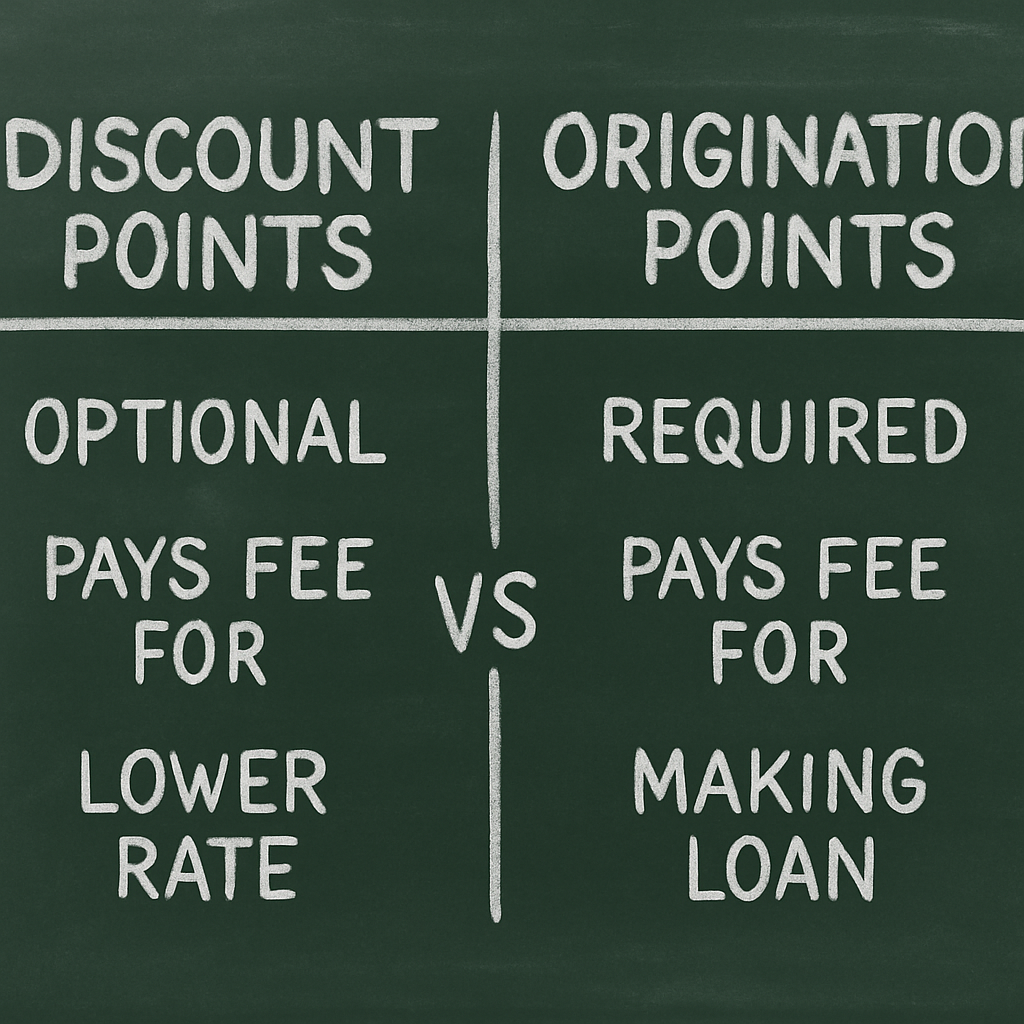

Before you hand over thousands of dollars, it is vital to understand that not all points are created equal. When getting loan points explained by a financial advisor, they will typically divide them into two distinct categories: discount points vs origination points.

Origination points are fees charged by the lender to cover the costs of processing, underwriting, and creating your loan. These points do not lower your interest rate; they are simply a cost of doing business with that specific financial institution. Fortunately, as the mortgage market has become more competitive, many lenders have moved away from charging flat origination points, opting instead for standard flat-fee closing costs.

When most real estate professionals talk about points on loans, they are referring to discount points. This is where the magic happens. A discount point is a fee you pay upfront in exchange for a permanently lower interest rate. This strategy is widely known as buying down interest rate mortgage.

Think of discount points as prepaid interest at closing. By handing the lender a lump sum of cash before you even move in, they reward you by charging you less interest every month for the rest of your loan term.

If you want to create an accurate mortgage cost breakdown, you need to know exactly how these points will impact your closing costs.

As established earlier, the cost is strictly tied to your loan size. Let’s look at how much does one point cost across different mortgage amounts:

Keep in mind that you do not have to buy whole points. Lenders offer fractional points. You could buy 0.5 points (which would be 0.5% of the loan amount) or 1.25 points.

But how much does a point actually reduce your rate? Generally, paying points to lower interest rate yields a rate reduction of about 0.25% per point. So, if your initial quote is a 6.5% interest rate and you purchase one discount point, your new rate would drop to 6.25%.

Why would anyone willingly hand over an extra $3,000 or $5,000 at closing? There are two primary benefits to this strategy.

First, it is incredibly effective for lowering monthly mortgage payments. A lower interest rate means a lower monthly bill. This can give your household budget more breathing room month to month, freeing up cash for home repairs, utilities, or investments.

Second, it is a powerful tool for reducing long term interest costs. While it hurts to part with several thousand dollars at the closing table, the total interest you save over a 30-year term usually far exceeds the upfront cost.

So, should you pull the trigger and pay for points? The answer depends entirely on a mathematical concept known as the break-even point.

Calculating break even point mortgage is the process of figuring out exactly how many months it will take for your monthly savings to surpass the upfront cost of the point. Once you cross this timeline, every dollar you save is pure profit.

Here is a step-by-step example: Imagine you are borrowing $400,000.

To find your break-even point, divide the upfront cost by the monthly savings: $4,000 ÷ $66 = 60.6 months (just over 5 years).

If you plan to live in this house and keep this specific loan (without refinancing) for more than 5 years, buying the point is a brilliant financial move. If you plan to sell the house or refinance in 3 years, you will lose money on the deal. This calculation is the ultimate deciding factor when buyers ask their realtors, “in terms of a loan what is a point, and is it worth it?”

When reviewing your Loan Estimate, your loan officer will likely present you with a few different scenarios, usually framing the conversation as mortgage points vs no points.

Choose to Buy Points If:

Choose NO Points If:

When trying to decide, “should I buy points on a mortgage?”, always base your choice on your personal time horizon. The longer you hold the mortgage, the more valuable points become.

What if you are completely strapped for cash at closing? You can actually utilize points in reverse.

Instead of paying discount points to lower your rate, you can accept a higher interest rate in exchange for lender credits for closing costs. Also known as “negative points,” this setup involves the lender covering some or all of your closing costs upfront. In return, you agree to a higher monthly payment.

This is a fantastic strategy if you want to keep your cash in your pocket today, or if you plan to flip the house or refinance in just a year or two.

The real estate market moves fast, and interest rates fluctuate daily. When you finally find a rate and a point structure you like, you will utilize a rate lock.

Mortgage rate locks and points go hand in hand. When you lock your rate with your lender (usually for 30 to 60 days), you are also locking in the cost of the points required to get that rate. This protects you from market volatility. If national rates spike before your closing day, your lower rate—and the price you agreed to pay for those points—remains completely secure.

For the financially savvy homeowner, points offer a few more layers of complexity that are worth noting.

First, a common question among buyers is: are mortgage points tax deductible? The short answer is yes, they often are. Because the IRS views discount points as prepaid interest, they are generally deductible in the year you pay them, provided you are using the loan to buy, build, or substantially improve your primary residence. (Origination points, however, are usually not deductible). Always consult with a certified tax professional to see how this applies to your specific tax bracket.

Secondly, you should be aware of the impact of points on APR (Annual Percentage Rate). Your APR is different from your interest rate; it represents the true, total cost of borrowing money over a year, inclusive of fees. Because paying points increases your upfront costs, it will alter your APR. While the nominal interest rate drops, the APR reflects the large lump sum paid at closing, giving you a more holistic view of the loan’s true cost.

The world of real estate finance doesn’t have to be intimidating. So, the next time a friend or family member asks you, “in terms of a loan what is a point?”, you can confidently explain the mechanics.

To recap:

Understanding these concepts gives you incredible leverage at the negotiating table. Whether you choose to pay points to secure a rock-bottom rate, take a zero-point loan for flexibility, or opt for lender credits to save cash today, you are now equipped to make the best, most cost-effective decision for your financial future.