Let's Shape The Future Of Your Investments!

Natoque iaculis cursus augue urna commodo aptent morbi tortor porttitor quis ornare.

In today’s dynamic financial landscape, achieving financial freedom often comes down to mastering the art of high yield investing. If you frequently find yourself wondering where to invest money to get good returns, you certainly aren’t alone. Between fluctuating market conditions and shifting economic policies, investors are actively searching for the best investments right now to maximize their wealth.

Whether you are a young professional trying to build a robust portfolio or someone nearing the end of their career, understanding your investment options is paramount. True wealth generation isn’t just about picking a single winning stock; it requires a strategic approach to capital allocation.

Before diving into specific asset classes, it is vital to understand the fundamental difference between passive income vs capital appreciation. Capital appreciation occurs when an asset—like a stock or a piece of real estate—increases in value over time. You only realize this gain when you sell the asset.

Passive income, on the other hand, is the money your investments generate on a regular basis without requiring you to sell off the underlying asset. High yield investing focuses heavily on this income-generation side of the equation. By prioritizing yield, investors can create a sustainable financial ecosystem that excels at protecting purchasing power against inflation. Cash flow gives you agility; it provides funds you can either live on or reinvest, regardless of whether the broader stock market is up or down.

When considering different ways to invest money for yield, the financial markets offer a rich variety of vehicles. The key is to match the yield potential with your personal risk tolerance.

One of the most popular avenues for generating cash flow is the stock market, specifically through dividend-paying companies. But not all dividends are created equal.

For steady, reliable growth, many investors look to dividend aristocrats. These are S&P 500 companies that have not only paid consistently but have increased their base dividend payout for at least 25 consecutive years. These companies typically have robust, recession-resistant business models.

When exploring equities, it is also important to understand the mechanics of preferred shares vs common stock dividends. Common stock dividends can fluctuate based on a company’s quarterly earnings and management’s discretion. Preferred shares, however, function more like a hybrid between a stock and a bond. They offer fixed dividends that must be paid out before any dividends are issued to common shareholders, making them a more stable income play.

No matter which equity route you choose, the true magic happens when you practice compounding dividends for long-term growth. By automatically reinvesting your dividends to buy more shares, you increase your future dividend payouts, creating a snowball effect that can exponentially grow your portfolio over decades.

If you are looking for alternative ways of generating monthly cash flow from investments, real estate and private credit offer excellent yields.

Real Estate Investment Trusts (REITs): You don’t need to be a landlord to make money in real estate. REITs are companies that own, operate, or finance income-producing real estate. By law, they are required to distribute at least 90% of their taxable income to shareholders in the form of dividends. Keeping an eye on real estate investment trusts performance can reveal opportunities in sectors like healthcare facilities, data centers, and commercial warehousing, which often yield significantly higher returns than traditional index funds.

Business Development Companies (BDCs): For those seeking high yields, having business development companies explained is often a lightbulb moment. BDCs provide capital to small and mid-sized private businesses. Because traditional banks often ignore these “middle-market” companies, BDCs can charge higher interest rates on the loans they provide. Like REITs, BDCs pass the majority of this income directly to shareholders, frequently resulting in dividend yields of 7% to 10% or more.

Bonds have historically been the bedrock of income investing. However, navigating the corporate debt market requires diligence, particularly when it comes to evaluating credit ratings of corporate debt.

Agencies like Moody’s and Standard & Poor’s rate bonds based on the issuer’s financial health. Highly rated “investment grade” bonds offer safety but lower yields. To chase higher returns, investors often look to high-yield bonds. But newcomers frequently ask: what are the risks of junk bonds? Junk bonds (or high-yield bonds) are issued by companies with lower credit ratings. While they offer enticingly high interest rates, they carry a significantly higher risk of default.

To safely capture these higher yields, mitigating credit risk in bond funds is essential. Instead of buying individual high-yield bonds, you can invest in mutual funds or ETFs that pool thousands of bonds together. This diversification softens the blow if a single company defaults, which is a foundational rule of building a diversified fixed income portfolio.

Sometimes the best way to invest money is to prioritize absolute capital preservation while still earning a respectable return. In high interest-rate environments, cash equivalents become highly attractive investment opportunities.

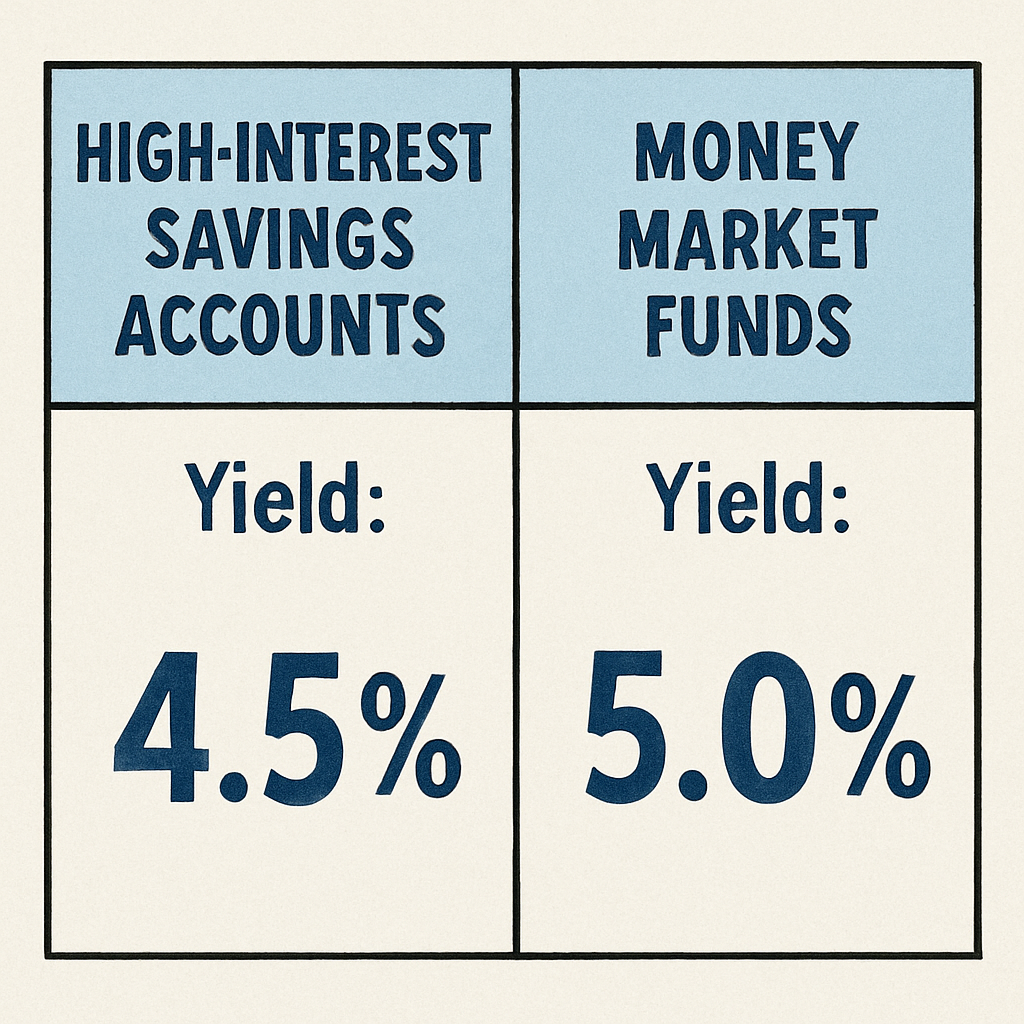

When deciding where to invest your short-term cash, you will likely weigh high-interest savings accounts vs money market funds.

Both options are currently stellar choices for investors who want a guaranteed yield without the volatility of the stock or bond markets.

To truly excel at high yield investing, you must understand the math behind your money. A critical skill is knowing how to calculate effective annual yield (EAY).

While the nominal interest rate tells you what a bond or account pays in a year, the EAY takes compounding into effect. The formula is: EAY = (1 + r/n)^n – 1, where ‘r’ is the stated interest rate and ‘n’ is the number of compounding periods per year. Understanding this helps you accurately compare an asset that pays dividends monthly against one that pays annually, ensuring you accurately pinpoint where to invest money to get good returns.

Finding the best income producing assets for retirees looks very different from a strategy designed for a 30-year-old.

If you are currently deciding on where to invest, here are a few actionable rules to keep you grounded as you explore various investment options:

Mastering high yield investing is about much more than just finding the highest percentage payout on a screen. It requires a thoughtful balance between risk and reward, a deep understanding of market mechanics, and a clear vision of your personal financial goals.

From analyzing the reliable history of dividend aristocrats to safely navigating the corporate bond market, there are countless ways to put your capital to work. By continuously educating yourself and adhering to disciplined diversification, you can build a resilient portfolio that not only generates substantial cash flow today but also secures your financial independence for the future. Take the time to evaluate your current portfolio, explore these high-yield avenues, and start making your money work harder for you.