Let's Shape The Future Of Your Investments!

Natoque iaculis cursus augue urna commodo aptent morbi tortor porttitor quis ornare.

Have you ever looked at your bank balance and asked yourself, “How can I grow my money?” If so, you are certainly not alone. In a world where the cost of living seems to rise daily, figuring out the absolute best way to grow money is a universal financial goal. True money growth is rarely the result of a get-rich-quick scheme; rather, it is the product of patience, discipline, and well-planned financial habits.

Many people believe that building wealth is reserved for the wealthy, but that is a myth. Whether you have fifty dollars or five thousand dollars to spare each month, learning how to make your money grow is an accessible skill.

This comprehensive guide will walk you through actionable, proven strategies for long-term wealth building. By the end of this article, you will have a clear roadmap for your financial future.

Before you begin exploring the stock market or purchasing property, you need a rock-solid financial foundation. Taking these initial steps ensures that when you do start investing, you will not have to derail your progress when life throws you a curveball.

The golden rule of personal finance is building an emergency fund first. Why? Because unexpected expenses—like a sudden medical bill, a car repair, or a temporary job loss—are inevitable. Without a financial safety net, you might be forced to sell your investments prematurely or, worse, take on high-interest credit card debt. Aim to save three to six months’ worth of living expenses in a liquid, easily accessible account.

Your emergency fund shouldn’t just sit under a mattress or in a traditional bank account earning 0.01% interest. This is where high-yield savings account advantages come into play. These accounts, typically offered by online banks, provide significantly higher interest rates than traditional brick-and-mortar institutions.

While a savings account won’t make you wealthy overnight, keeping your cash here is crucial for protecting purchasing power against inflation. If inflation rises, the cost of goods goes up. A high-yield account acts as a buffer, ensuring your cash doesn’t lose its underlying value while it sits safely waiting for an emergency.

Once your safety net is established, it is time to transition from saving to investing.

One of the most common barriers to entry is the misconception that you need thousands of dollars to begin. Fortunately, figuring out how to start investing with little money has never been easier. Thanks to modern financial technology, you can start with as little as $5.

If you want to know the true secret to money growth, look no further than compound interest. The compound interest benefits are often described as the “eighth wonder of the world.” Simply put, compound interest is the interest you earn on your original investment, plus the interest you earn on your accumulated interest.

Actionable Example: If you invest $200 a month at an average annual return of 8%, you won’t just have $72,000 after 30 years (your total contributions). Thanks to compounding, your portfolio could grow to over $300,000. Time is your greatest asset in the market, making it essential to start as early as possible.

Human emotion is often the enemy of investment success. To remove the temptation to “time the market,” prioritize an automatic investment plan setup. By automatically transferring a set amount of money from your checking account to your brokerage account every month, you ensure consistent progress. Out of sight, out of mind, and steadily growing.

If you are currently researching how to invest money, you must understand that there is no one-size-fits-all approach. Your strategy should be uniquely tailored to your lifestyle, goals, and nerves.

Before buying a single asset, a thorough risk tolerance assessment for investors is necessary. Risk tolerance is your ability and willingness to lose some of your original investment in exchange for the potential of greater returns.

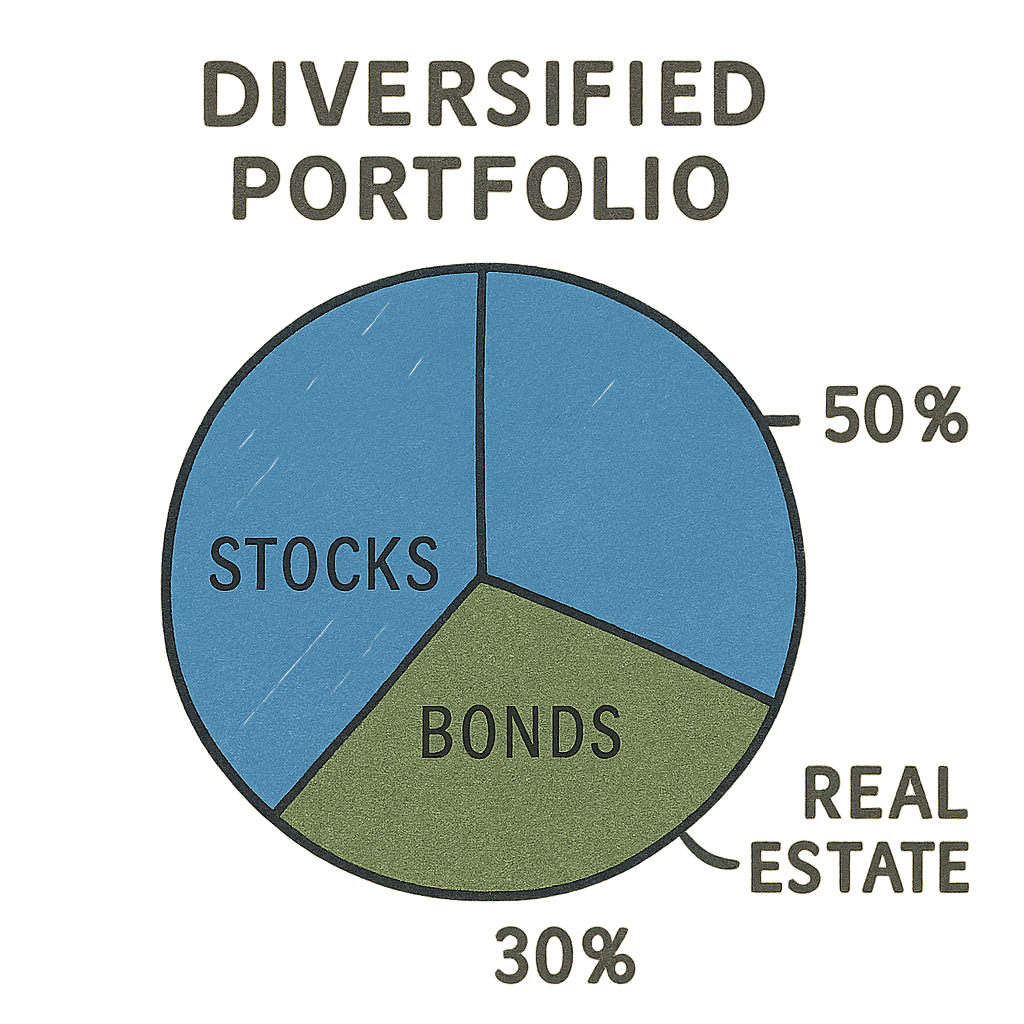

Never put all your eggs in one basket. A well-planned, diversified investment portfolio allocation spreads your money across different asset classes—such as large companies, small companies, international markets, and bonds. If one sector of the economy struggles, the others can help balance out your overall returns, reducing your total risk.

When deciding exactly what to buy, investors often face the debate of index funds vs individual stocks.

For the vast majority of retail investors, low-cost index funds are the smartest, most reliable path to long-term wealth. They offer instant diversification and historically outperform professional stock pickers over a 10-to-20-year timeline.

Markets go up and down daily. Trying to guess the perfect time to buy is a fool’s errand. Instead, rely on a proven technique. With dollar-cost averaging explained simply, it means investing a fixed dollar amount on a regular schedule, regardless of what the stock market is doing.

When the market is high, your fixed amount buys fewer shares. When the market is down and “on sale,” your fixed amount buys more shares. Over time, this averages out your purchase price and removes the anxiety of market volatility.

While the stock market is fantastic, there are other avenues when considering how can you invest money. Exploring alternative assets can further secure your financial future.

Actively working for a paycheck is just one way to earn. The wealthy focus heavily on creating passive income streams for beginners and experts alike. Passive income is money you earn that doesn’t require a lot of “active” daily effort to maintain.

Another massive pillar of wealth building is property. When comparing real estate vs stock market returns, both have distinct advantages.

The stock market offers high liquidity (you can sell shares instantly) and requires very little initial effort. Real estate, on the other hand, is generally less liquid but offers tangible value, tax write-offs, and monthly cash flow through rental income.

If buying a physical apartment building sounds too daunting or expensive, consider investing in REITs (Real Estate Investment Trusts). REITs trade on the stock market like regular companies but allow you to invest in large-scale, income-producing real estate without having to fix leaky toilets or deal with tenants.

Learning how to grow money is only half the battle. The other half is keeping it out of the hands of the taxman. Proper tax planning will significantly accelerate your journey to financial freedom.

The government incentivizes you to save for your future. Do not overlook the power of tax-advantaged retirement accounts like a 401(k) or an IRA (Individual Retirement Account).

If you invest in a standard brokerage account (one without special tax advantages), you will owe taxes on your profits when you sell an asset. This is called a capital gains tax.

A crucial strategy for minimizing capital gains taxes is to hold onto your investments for longer than one year. If you sell an asset after holding it for less than a year, you pay short-term capital gains tax, which is equivalent to your ordinary income tax rate (which can be quite high). If you hold the asset for over a year, you qualify for long-term capital gains tax rates, which are significantly lower (often 0%, 15%, or 20%, depending on your income). Patience literally pays off.

Finding the best way to grow money does not require a finance degree or a six-figure salary. It requires a fundamental shift in how you view your finances.

Start by protecting yourself with an emergency fund, harness the immense power of compound interest, and automate your investments to ensure consistency. By creating a diversified portfolio and taking advantage of tax-optimized accounts, you take control of your financial destiny.

Stop wondering, “How can I grow my money?” and start taking action today. Time is the most valuable asset you have in the market—use it wisely, stay disciplined through the market’s ups and downs, and watch your wealth grow over the decades to come.