Let's Shape The Future Of Your Investments!

Natoque iaculis cursus augue urna commodo aptent morbi tortor porttitor quis ornare.

Taking your first steps into the financial markets can feel like navigating a minefield. With the stock market’s constant ups and downs, it is entirely normal to feel hesitant about putting your hard-earned money on the line. If you are losing sleep over market fluctuations, you are likely searching for the best place to invest money without risk.

While all financial decisions carry some minute level of risk—even if it is just the risk of your money losing its purchasing power over time—there are several highly secure havens for your cash. Whether you are saving for a house down payment, building a rainy-day fund, or simply stepping back from the stock market, knowing where to invest cash safely is a crucial financial skill.

In this comprehensive guide, we will explore the safest investments available today, breaking down practical capital preservation strategies for conservative investors so you can grow your wealth with absolute peace of mind.

Before deciding on the best place to invest money without risk, it is essential to understand what “risk” actually means in finance. For beginners, risk usually means the possibility of losing the original money you put in (your principal). Therefore, protecting principal during market volatility becomes the primary objective.

However, conservative investors face two main challenges:

By balancing these two factors, you can find safe investment options that offer respectable yields without subjecting your portfolio to Wall Street’s rollercoaster. Let’s dive into the most reliable low risk investments available.

For absolute beginners, the banking sector provides the most accessible FDIC insured investment vehicles. If your bank is a member of the Federal Deposit Insurance Corporation (FDIC) or the National Credit Union Administration (NCUA), your deposits are federally backed up to $250,000 per depositor, per institution.

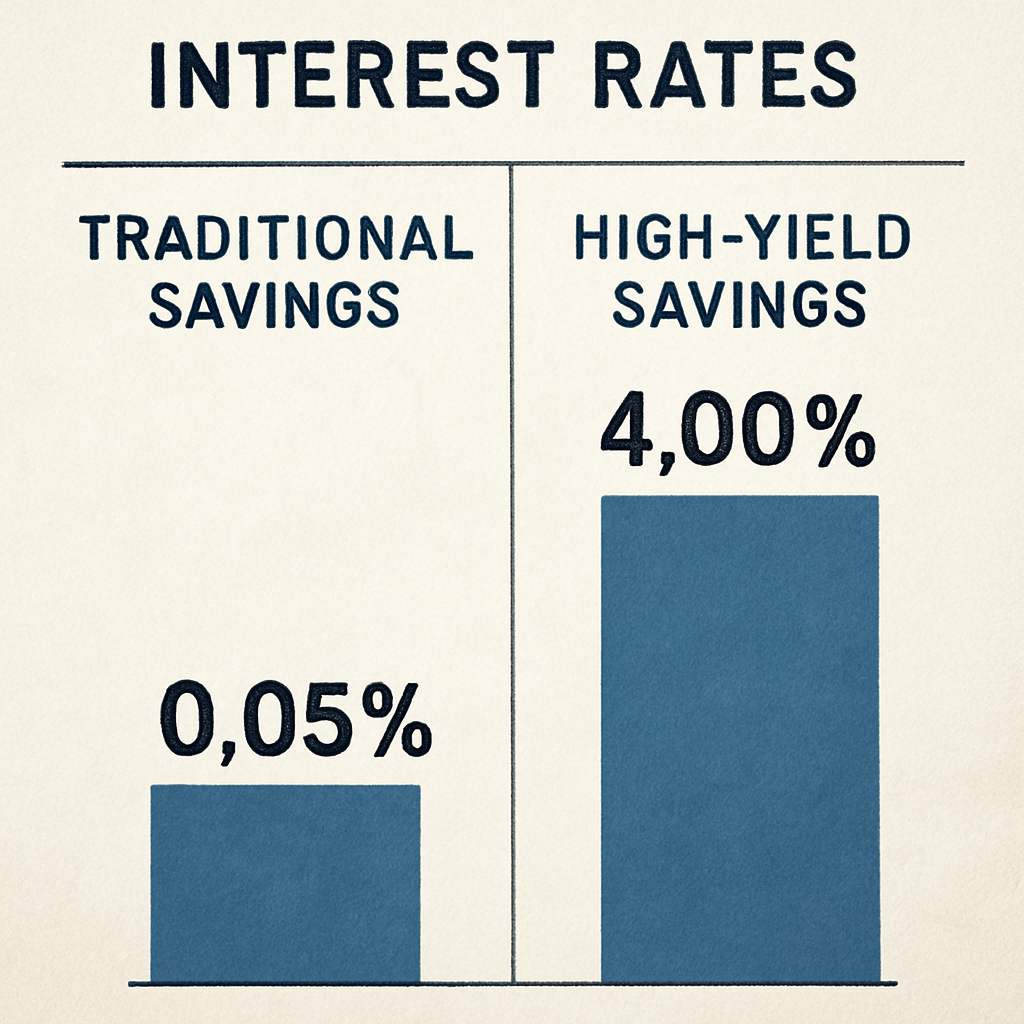

A common question from cautious beginners is: are high-yield savings accounts safe? The answer is a resounding yes. Provided you use an FDIC-insured institution, these accounts are practically immune to market crashes.

HYSAs operate exactly like traditional savings accounts, but because they are typically offered by online banks with lower overhead costs, they offer significantly higher interest rates.

When comparing CDs vs money market accounts, you are looking at two excellent, low-risk banking products that serve slightly different purposes.

Money Market Accounts (MMAs): MMAs are essentially a hybrid between a checking and a savings account. They offer higher interest rates than traditional savings accounts and usually come with a debit card or check-writing privileges. However, they often require a higher minimum balance. If you want a slight bump in yield while maintaining immediate access to your funds, MMAs are fantastic safe investments.

Certificates of Deposit (CDs): A CD requires you to leave your money untouched for a predetermined term (e.g., 6 months, 1 year, or 5 years). In exchange for giving up liquidity, the bank guarantees a fixed interest rate. This makes CDs one of the top guaranteed return on investment options. If interest rates drop across the broader economy, your CD rate remains locked in.

When financial experts talk about the safest investments in the world, they are usually referring to debt issued by the United States government. Because the U.S. government has never defaulted on its debt, these are considered the ultimate low-risk alternatives to stocks.

If you want to step outside of standard bank accounts, exploring fixed income securities for beginners is your next logical step.

When navigating government debt, you will often find yourself comparing Treasury bills vs savings bonds. Both are backed by the full faith and credit of the U.S. government, but they function differently.

Treasury Bills (T-Bills): T-Bills are short-term government debt obligations with maturities ranging from 4 weeks to 52 weeks. They are sold at a discount to their face value. For instance, you might buy a $1,000 T-Bill for $950; when it matures, the government pays you the full $1,000.

Savings Bonds (Series EE and Series I): Unlike T-bills, savings bonds are designed for longer-term holding. They cannot be cashed in for at least one year, and if you cash them in before five years, you lose the last three months of interest.

One of the most popular government assets in recent years has been the Series I Bond. These unique bonds are specifically designed to answer the question of how to protect savings from inflation.

The interest rate on an I-Bond consists of two parts: a fixed rate that stays the same for the life of the bond, and an inflation rate that adjusts twice a year based on the Consumer Price Index. Because Series I Savings Bonds rates rise when inflation rises, they ensure your money maintains its purchasing power.

Knowing where to invest cash is only half the battle. How you structure those investments determines whether you achieve the best return on investment possible within the low-risk category.

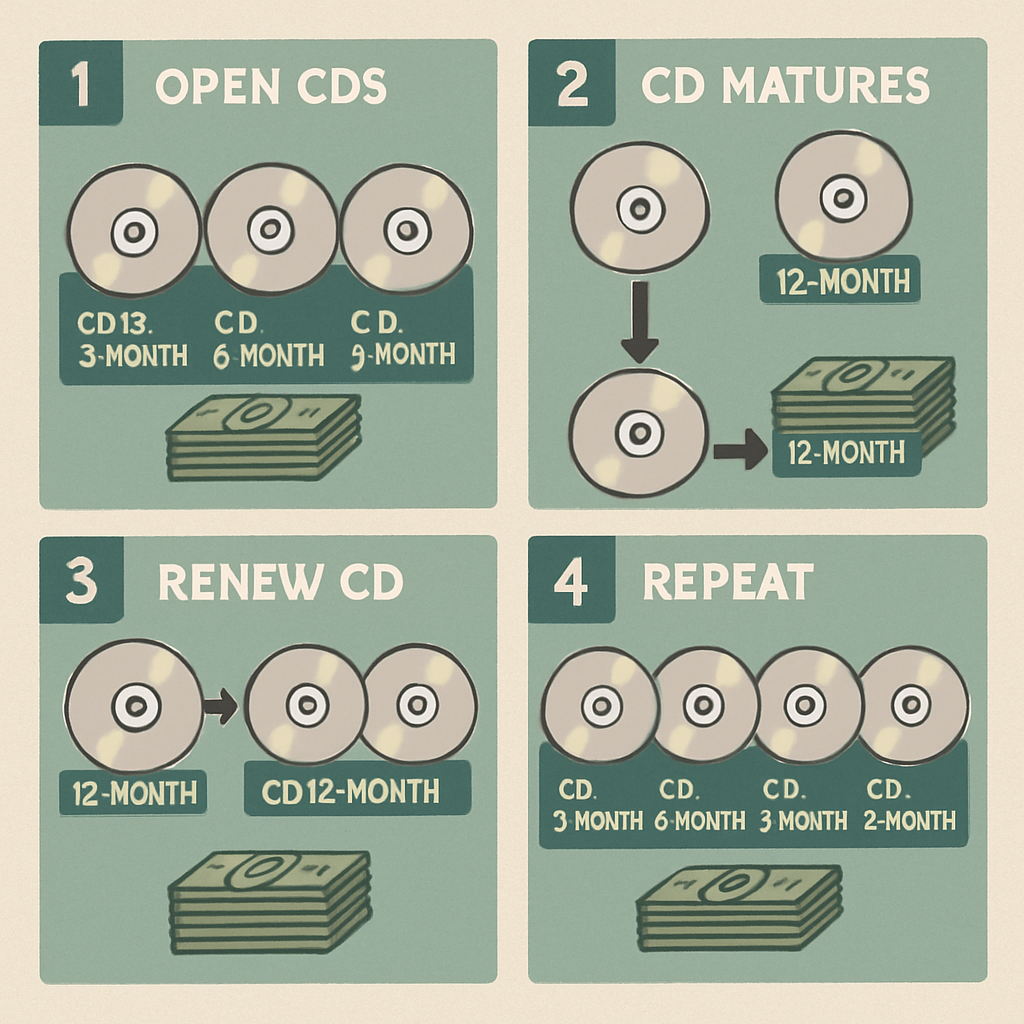

One of the most effective strategies for conservative investors is a “ladder.” Because of the liquidity vs interest rate trade-off, locking all your money into a 5-year CD might earn you a high rate, but it leaves you without accessible cash.

Building a risk-free laddering strategy solves this. Here is how you can build a simple 12-month CD ladder:

As each CD matures, you take that money (plus the interest) and reinvest it into a new 12-month CD. Eventually, you will have a 12-month CD maturing every three months. This grants you regular access to your cash without sacrificing the higher interest rates of longer-term deposits. You can do the exact same thing with Treasury bills!

If you have a major expense coming up within the next year—like a wedding, a tax bill, or a tuition payment—the stock market is not the place for those funds. A 10% market correction right before your bill is due could be financially disastrous.

For timelines under a year, your safe investment options should be restricted to:

These instruments ensure that your principal is protected, fulfilling the core mandate of capital preservation strategies for conservative investors.

A common misconception among beginners is that choosing safe investments means accepting near-zero growth. While it is true that you won’t see the 10% to 15% annual gains sometimes offered by aggressive stock portfolios, today’s high-interest-rate environment means you can secure returns of 4% to 5% (or more) with essentially zero risk of losing your principal.

When looking for the best return on investment in the low-risk tier, always shop around. Online banks consistently offer better yields than traditional brick-and-mortar mega-banks. Furthermore, utilizing platforms like TreasuryDirect allows you to buy government securities directly without paying broker fees.

Remember, the goal of these low risk investments isn’t to make you a millionaire overnight. The goal is stability. By utilizing these guaranteed return on investment options, you create a solid financial bedrock. Once your emergency fund is secure and your short-term cash is safely parked and earning interest, you may find that you finally have the financial confidence to take calculated risks with the rest of your portfolio.

Finding the best place to invest money without risk doesn’t have to be complicated. Whether you are utilizing the flexibility of an HYSA, taking advantage of FDIC insured investment vehicles like CDs, or relying on the time-tested security of U.S. Treasury bills, you have multiple pathways to safely grow your wealth.By understanding your own timeline, recognizing the impact of inflation, and deploying smart tactics like a laddering strategy, you can confidently protect your capital from market storms. Evaluate your current cash reserves today, choose the safe investment options that align with your financial goals, and let your money start working for you—securely and reliably.