Let's Shape The Future Of Your Investments!

Natoque iaculis cursus augue urna commodo aptent morbi tortor porttitor quis ornare.

Loans are a common part of financial life. They help people achieve goals like buying a home or funding education.

But how do loans work? Understanding the basics can be crucial for making informed decisions.

A loan is essentially borrowed money that must be repaid with interest. This interest is the cost of borrowing.

Loans come in various forms, each with its own terms and conditions. Knowing these can prevent financial pitfalls.

In this guide, we’ll explore loan mechanics, definitions, and processes. You’ll learn how to navigate the world of borrowing.

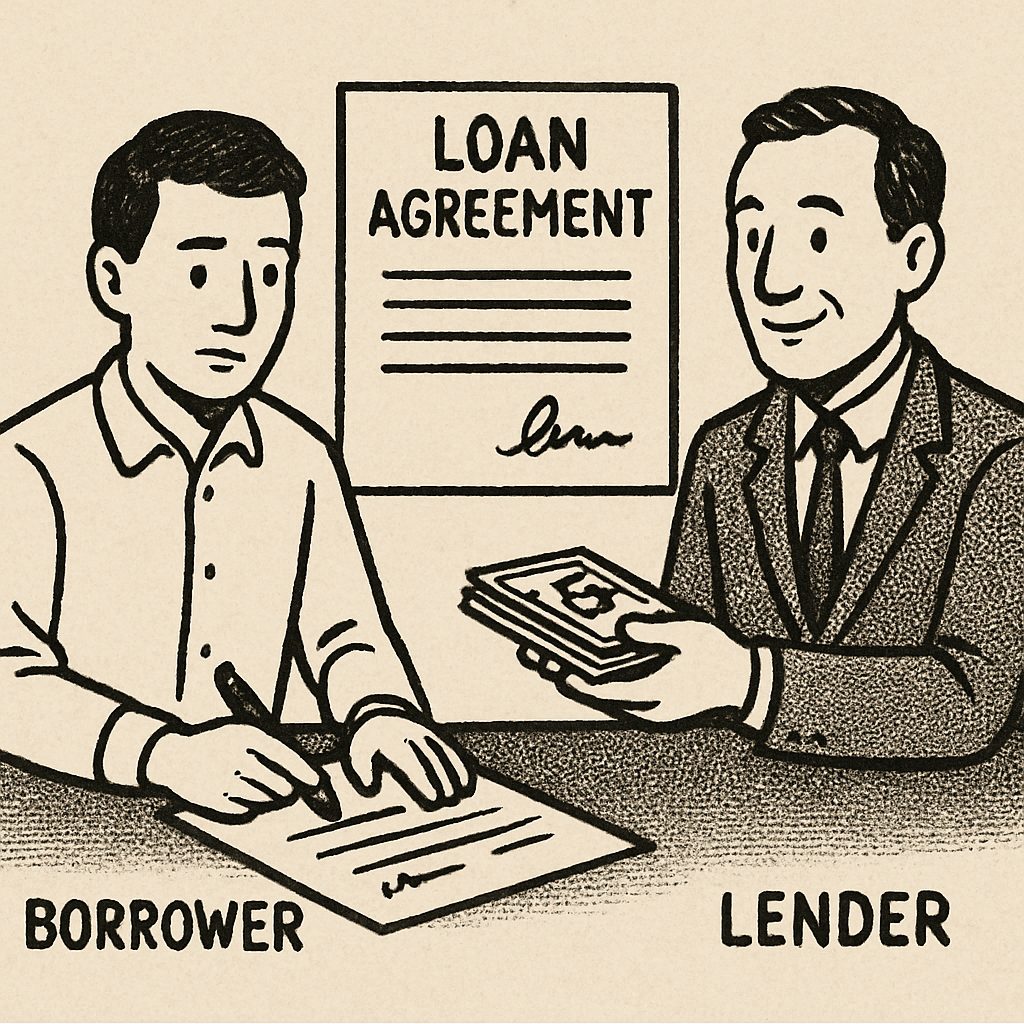

A loan is an agreement between a borrower and a lender. The borrower receives money with the promise to repay it, plus interest. This arrangement allows individuals to access funds for various needs.

The loan meaning extends beyond just borrowing money. It involves understanding terms like the principal, interest, and repayment period. The principal is the initial amount borrowed. Interest is the extra cost paid for using the lender’s money.

Here’s a simplified definition of a loan:

Understanding what a loan entails is essential for smart financial management. It helps borrowers plan their finances and avoid pitfalls. By defining a loan in its simplest terms, individuals can make informed decisions and utilize loans as effective financial tools.

Understanding how loans work begins with knowing the loan process. The process starts when a borrower submits a loan application to a lender. This application includes details about income, expenses, and credit history.

Once the application is received, the lender evaluates the borrower’s creditworthiness. This involves checking credit scores and verifying income. A good credit score can lead to better loan terms.

If approved, the borrower is presented with a loan offer. This offer details the loan’s terms, such as the amount, interest rate, and repayment schedule. It’s crucial to review these terms carefully.

The loan process can be summarized in these steps:

Once the terms are accepted, funds are disbursed to the borrower. Repayment begins according to the agreed schedule. Understanding each step of this process ensures borrowers are prepared and able to meet their financial obligations.

When analyzing loans, three main components are essential: principal, interest, and loan terms. Each of these elements plays a critical role in understanding the overall loan mechanism.

The principal refers to the original amount borrowed from the lender. It’s the base figure upon which interest is calculated. For instance, in a $10,000 loan, the principal is $10,000.

Interest is the cost of borrowing money, charged as a percentage of the principal. It compensates the lender for the risk of lending. Rates can vary depending on creditworthiness and the loan type.

Loan terms encompass the details surrounding repayment, including the duration and payment schedule. Terms can also outline conditions such as fees or penalties. Understanding these terms is key to informed borrowing decisions.

To summarize the key components:

Grasping these components helps borrowers comprehend the full cost and obligations of a loan. It’s essential to evaluate each part for a well-rounded financial decision.

Loans come in various types, each serving different needs and conditions. Understanding these differences can aid in selecting the right loan for your circumstances.

Secured loans are backed by collateral. This collateral might be property, a vehicle, or other assets. If you default, the lender can seize the collateral to recover losses. Mortgages and auto loans are common examples of secured loans.

Unsecured loans do not require collateral. Instead, these loans are granted based on the borrower’s creditworthiness. Credit cards and personal loans often fall into this category. However, they may carry higher interest rates due to increased risk for the lender.

Beyond secured and unsecured loans, others are designed for specific purposes. Student loans, for instance, help finance education. Business loans fund company growth and operations. Each type has unique terms and conditions.

To better understand these loan categories:

by Sasun Bughdaryan (https://unsplash.com/@sasun1990)

Recognizing these loan types can guide you in making informed financial choices. Each loan is a tool to achieve distinct goals while managing financial risks effectively.

Interest rates are a crucial part of borrowing. They affect how much you ultimately repay over the loan’s lifespan. Choosing between fixed and variable rates depends on financial goals and risk tolerance.

Fixed interest rates remain constant for the entire loan term. This provides stability and predictability in payments. Borrowers with fixed rates can plan budgets easily, with no surprises from rate changes.

Variable interest rates, however, can fluctuate. They’re often tied to market conditions or an index. While initial rates might be lower, payments can increase if rates rise. This option suits those who can handle potential payment shifts.

When considering interest rates, weigh the pros and cons of each:

by Leon Hu (https://unsplash.com/@leonhu123)

Understanding these rate types aids in aligning loan choices with financial comfort and long-term planning. Be sure to carefully evaluate which is suitable before committing to a loan.

Applying for a loan involves several detailed steps. This process ensures you qualify for the amount you wish to borrow. Lenders need assurance that you can repay the loan as agreed.

The first step is gathering necessary documents. This often includes proof of income, identification, and possibly collateral. Proper documentation enhances your approval chances and expedites the process.

Lenders will assess your credit score and history. They evaluate your creditworthiness and determine suitable interest rates. A higher credit score often leads to better terms.

Understanding lender requirements is crucial. Here are typical steps in the loan application process:

Each step provides valuable insights into a borrower’s financial health. Being prepared and informed can streamline the application and lead to more favorable outcomes.

Repaying a loan involves more than just making monthly payments. Understanding your repayment schedule is crucial. It helps in budgeting and ensures timely payments.

Most loans have structured monthly installments. These installments consist of both principal and interest. Knowing how much goes to each component can help manage your finances better.

Different repayment methods are available. Some borrowers prefer automatic deductions. Others choose manual payments for more control over timing. Selecting the right method depends on personal financial habits.

Here are some tips for effective loan repayment:

Adhering to your repayment plan maintains good credit health. It also reduces financial stress in the long run. Planning and discipline are key to successful loan management.

When borrowing money, it’s essential to be aware of additional costs. These costs can significantly affect the overall expense of your loan. Hidden fees are common in many loan agreements.

Understanding potential fees allows for smarter financial planning. Origination fees, for example, are charged for processing your loan application. Be sure to check for these in your agreement.

Penalties can also arise if you default or pay off loans early. Being aware of these possibilities can prevent unpleasant surprises. Here are some common costs to watch out for:

These additional costs may not seem significant at first. However, they can add up over time. Always read the fine print in loan agreements to fully understand all potential expenses. This knowledge can help you avoid unnecessary financial burdens.

Loans play a pivotal role in shaping your credit history. Timely payments reflect positively on your credit score, boosting your financial reputation. On the flip side, late payments can harm your score significantly.

Credit scores influence loan eligibility and terms. A higher score generally leads to better loan offers and lower interest rates. Thus, understanding loans can empower your financial decisions.

Beyond credit, loans impact overall financial health. They can help achieve goals but also create burdens if mishandled. Keep track of the following to maintain stability:

Monitoring these factors helps in maintaining healthy credit and managing debt wisely. Planning and financial education are keys to leveraging loans for growth.

Loan calculators are vital tools for planning your borrowing strategy. They can estimate monthly payments and total loan costs. This aids in evaluating if a loan fits your budget.

Additionally, comparing loan offers is essential. It ensures you secure the best deal with favorable terms. Consider the following when evaluating offers:

Utilizing these resources helps make informed borrowing decisions and choose the right loan for your needs.

When considering a loan, many questions arise. It’s important to have clear answers to make informed choices. Understanding the basics can clarify the borrowing process.

Here are a few common loan-related questions:

These queries are just the tip of the iceberg. Each answer can significantly impact your financial planning and decision-making. Seeking advice from financial experts or reading detailed guides can provide clarity and confidence.

Making informed decisions about loans requires understanding the fundamental concepts. Awareness of loan types, interest rates, and repayment terms is essential. A strong grasp of these mechanics helps avoid financial pitfalls and ensures successful borrowing.

Stay informed and proactive when considering loan offers. This mindset empowers you to choose the best options and align them with your financial goals. By doing so, you protect your financial health and future stability.