Let's Shape The Future Of Your Investments!

Natoque iaculis cursus augue urna commodo aptent morbi tortor porttitor quis ornare.

Driving offers incredible freedom, but it also comes with undeniable risks. Even the most cautious, experienced drivers can find themselves facing unexpected hazards on the road. Whether it is a slick street during a rainstorm, a distracted driver running a red light, or an unavoidable pothole, accidents happen. When they do, having the right financial protection is essential, and this is exactly where collision car insurance steps in to save the day.

If you are navigating the complex world of auto policies, you might find yourself overwhelmed by the industry jargon. What protections are required? What is optional? And most importantly, what actually protects your hard-earned assets?

In this comprehensive guide, we will break down everything you need to know about protecting your vehicle, from understanding limits and deductibles to navigating the claims process.

To start, let us answer a fundamental question: what is collision insurance?

In the simplest terms, the core collision insurance meaning refers to an auto insurance policy designed to help pay for the repair or replacement of your vehicle if it is damaged in an accident with another vehicle or an object.

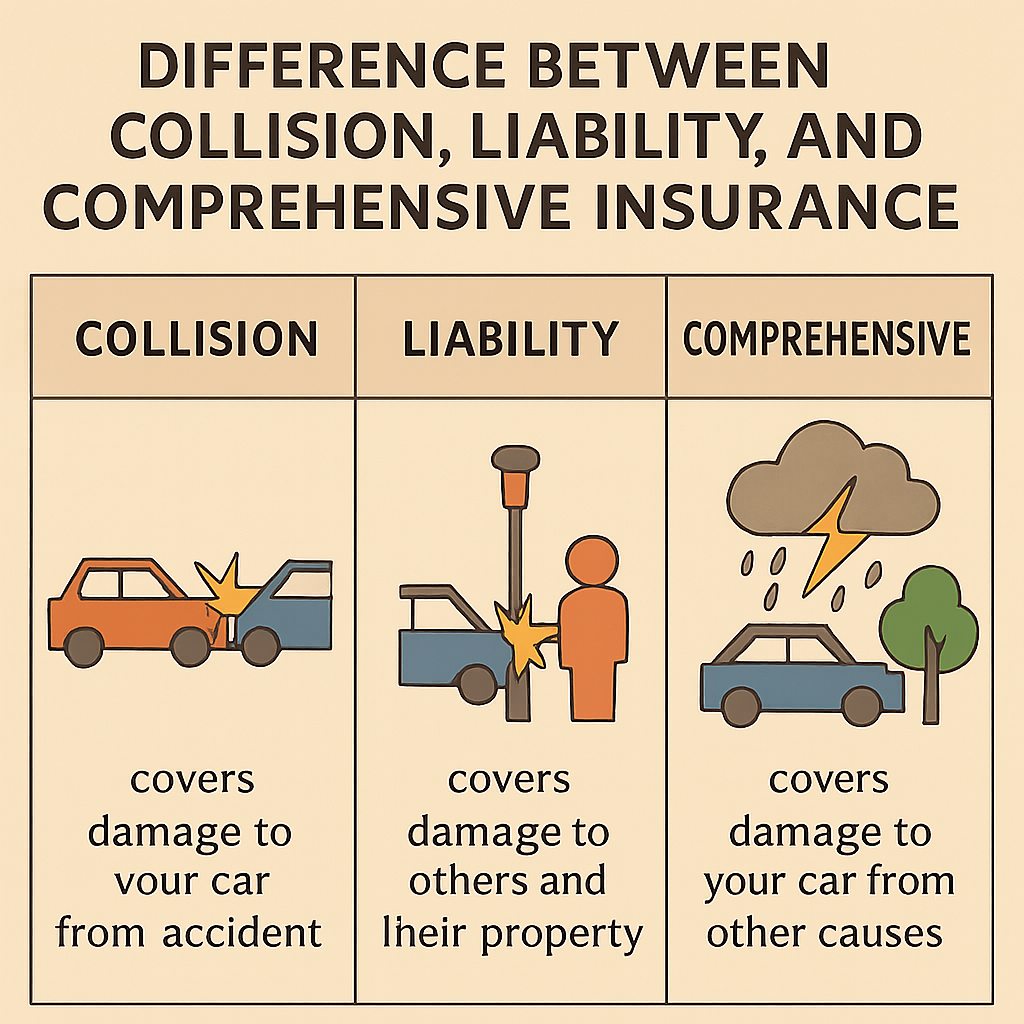

When you ask an agent, “what is collision coverage going to do for me?” they will explain that it focuses specifically on your car, regardless of who is to blame for the accident. While your liability insurance covers the damage you cause to other people and their property, collision auto insurance exists solely to protect your vehicle.

Understanding exactly what does collision insurance cover is crucial so you do not face unwelcome surprises after an accident. To adequately cover collision events, this policy steps in during several common scenarios:

Note: Collision coverage does not pay for medical bills, damage to another person’s vehicle, or non-driving-related damage (like hail or theft).

When building an insurance policy, it is easy to get coverages mixed up. To make informed decisions, it is helpful to look at how collision fits into the bigger picture.

A quick liability vs full coverage comparison reveals a stark difference in protection. Liability insurance is legally required in almost every state; however, it only pays for the injuries and property damage of the other party if you cause a crash. It leaves you entirely responsible for your own repair bills.

“Full coverage” is not a single type of insurance, but rather an industry term for a policy that includes Liability, Comprehensive, and Collision coverage combined.

Many drivers confuse these two optional coverages. When comparing comprehensive and collision protections, the easiest way to remember the difference is by the type of event:

Before your insurance provider pays a dime toward your repairs, you must navigate deductibles and vehicle valuations.

Your deductible is the out-of-pocket amount you agree to pay before your insurance coverage kicks in. Selecting the right deductible amount requires a careful balancing act between your monthly budget and your emergency savings.

If you choose a high deductible (e.g., $1,000), your monthly premium will be lower. However, you must have $1,000 readily available in case of a crash. Conversely, a lower deductible (e.g., $250) means higher monthly premiums but less financial strain immediately following an accident.

When you file a claim, insurance companies do not just write a blank check. Understanding actual cash value vs replacement cost is critical here.

Most standard collision policies pay out the Actual Cash Value (ACV) of your vehicle, not what it would cost to buy a brand-new replacement. The ACV is calculated by determining your car’s original purchase price and subtracting depreciation based on age, mileage, and wear and tear.

When estimating vehicle market value for insurance purposes, adjusters look at recent sales of similar vehicles in your local area, the pre-crash condition of your car, and historical depreciation rates.

Accidents vary in severity. A minor fender bender might require a new bumper, but a high-speed crash can structurally compromise the entire car. This leads many drivers to ask: what happens if my car is totaled in an accident?

Your insurance company will not pay more to fix a car than the car is actually worth. Insurance adjusters will always analyze car repair costs versus total loss valuation to make this decision.

If the cost to repair your vehicle reaches a certain percentage of its Actual Cash Value (often between 70% and 80%, depending on state laws and insurer policies), the insurance company will declare the vehicle a “total loss.” Instead of paying a mechanic, they will cut you a check for the ACV of the car, minus your deductible.

If you do not own your car outright, you have additional rules to follow. You must be strictly aware of auto lender insurance requirements. Banks and leasing companies almost universally require you to carry both collision and comprehensive insurance until the vehicle is completely paid off. This protects their financial investment in the asset.

Furthermore, because vehicles depreciate quickly, you might owe more on your loan than the car’s ACV. If your car is totaled, the insurer’s payout might leave you thousands of dollars short of paying off the lender. This is where gap insurance for financed vehicles becomes a financial lifesaver. Gap insurance covers the “gap” between what you owe on your auto loan and the actual cash value payout you receive from your collision policy.

Because collision coverage is generally optional (unless mandated by a lender), drivers must evaluate whether the ongoing cost is worth the protection.

A very common dilemma is deciding: is collision coverage worth it for old cars? As a vehicle ages and its mileage increases, its actual cash value drops significantly.

Financial advisors often recommend the “10% Rule.” If your annual cost for comprehensive and collision insurance exceeds 10% of your vehicle’s total market value, it might be time to drop the coverage. For example, if you have a 15-year-old sedan worth $2,000, and your collision coverage costs $300 a year, you are paying a massive premium for a relatively tiny maximum payout (especially after factoring in a $500 deductible). In this scenario, putting that $300 into a savings account for future repairs or a down payment on a new car is likely the smarter financial move.

No one likes paying high insurance bills. Fortunately, decreasing monthly premiums through policy adjustments is an actionable step any driver can take.

You also need to understand how at-fault accidents impact premium rates. When you file a collision claim for an accident where you were at fault, your insurer views you as a higher risk. This almost always results in a premium increase upon your policy renewal. In some cases, if the damage is incredibly minor (like a $600 scratch) and you have a $500 deductible, it might be cheaper in the long run to pay out of pocket rather than file a claim and face years of increased rates.

If the worst happens and you need to use your coverage, knowing exactly how to file a vehicle damage claim will save you immense stress.

Navigating the roads safely is a priority for every driver, but having a financial safety net is just as critical. Collision car insurance provides unparalleled peace of mind, ensuring that an unexpected encounter with a guardrail, a pothole, or another driver doesn’t completely derail your finances.

By understanding the exact details of your policy—from deductibles and vehicle valuations to how claims impact your future premiums—you empower yourself to make the best possible decisions for your vehicle and your wallet. Take the time today to review your current auto policy, assess the true value of your car, and ensure you have the optimal level of protection for the road ahead.